Fill in a Valid Oklahoma 501 Template

The Oklahoma 501 form serves as an essential tool for reporting various types of income to the Oklahoma Tax Commission. This annual information return is required for a range of payors, including organizations like churches, labor unions, and even state departments. Individuals, partnerships, and corporations must complete this form to report payments that meet or exceed specific thresholds, such as $750 for interest or rental payments. The form requires details such as the type of entity submitting the return, the tax year, and the federal identification or social security number. Importantly, the Oklahoma 501 form must be submitted by February 28 of the year following the reporting year, although certain payments, such as those made to nonresident royalty owners, have an earlier deadline of January 31. Each type of income reported requires a separate form, and payors must ensure they comply with the state's guidelines on what constitutes reportable income. This includes not only traditional income sources but also production payments related to mineral interests in Oklahoma. By adhering to these requirements, payors help maintain transparency and compliance within the state's tax system.

Document Properties

| Fact Name | Details |

|---|---|

| Purpose | The Oklahoma 501 form is used for reporting various types of income payments made by payors to individuals or organizations. |

| Filing Deadline | Returns must be submitted to the Oklahoma Tax Commission by February 28 of the following year, with some exceptions for specific payments. |

| Applicable Laws | This form is governed by Title 68 O.S. Sections 2385.26 and 2385.30, which outline the requirements for reporting income payments. |

| Who Must File | All payors, including organizations like churches, schools, and government entities, are required to report payments using this form. |

| Payment Threshold | Payments of $750 or more must be reported, with specific thresholds for certain types of income, such as dividends and interest. |

| Nonresident Reporting | Payments made to nonresidents totaling $750 or more must also be reported, especially if the income is generated from Oklahoma sources. |

| Mailing Address | Completed forms and reports should be mailed to the Oklahoma Tax Commission at 2501 North Lincoln Blvd., Oklahoma City, OK 73194-0009. |

Common mistakes

-

Incomplete Identification Information: Many individuals fail to provide complete identification details, such as the Federal Identification Number or Social Security Number. This omission can lead to delays in processing the form.

-

Incorrect Tax Year: Submitting the form with the wrong tax year is a common mistake. Ensure the tax year is accurately filled in to avoid complications with the Oklahoma Tax Commission.

-

Not Indicating the Type of Form: It is crucial to check only one box to indicate the type of form being transmitted. Failing to do so can result in the form being rejected or returned for correction.

-

Missing Signature: A signature is required to validate the form. Many individuals neglect this step, which can lead to the form being considered incomplete.

-

Improper Mailing: Sending the form to the wrong address or failing to send it by the due date can lead to penalties. Ensure it reaches the Oklahoma Tax Commission by February 28 or the specified due date for your situation.

Popular PDF Documents

New Hire Reporting Oklahoma - Forms that are incomplete may delay processing and compliance checks.

Oklahoma Wc 12 - Applicants should keep a copy of the submitted form for their records.

To ensure a smooth transaction when buying or selling a recreational vehicle, it is crucial to utilize a Texas RV Bill of Sale form. This document acts as a safeguard for both parties involved, providing clear evidence of the ownership transfer. For those looking to access or learn more about this form, a valuable resource is UsaLawDocs.com, where you can find additional information and templates to facilitate the process.

Oklahoma Real Estate Contract Pdf - Covenants, easements, and property use restrictions are necessary to include during title examination.

Misconceptions

Here are six common misconceptions about the Oklahoma 501 form, along with clarifications to help understand its purpose and requirements.

- Only businesses need to file the Oklahoma 501 form. Many individuals, including those receiving certain types of income, must also submit this form. This includes individuals, trusts, and estates.

- The Oklahoma 501 form is only for reporting payments to residents. In fact, payments made to nonresidents must also be reported if they meet the specified thresholds.

- Payments under $750 do not need to be reported. While many payments below this amount may not require reporting, specific types of income, such as royalties, have different thresholds, such as $10.

- Filing the Oklahoma 501 form means you must pay taxes immediately. The form is an information return, and no payment is required at the time of filing. It is essential to follow the instructions for payment separately if needed.

- Only certain types of organizations can submit the form. The requirement to file applies to a wide range of payors, including churches, charitable organizations, and even individuals who make qualifying payments.

- All forms can be submitted on one Oklahoma 501. Each type of statement requires a separate Oklahoma 501 form. It is important to indicate the type of payment being reported accurately.

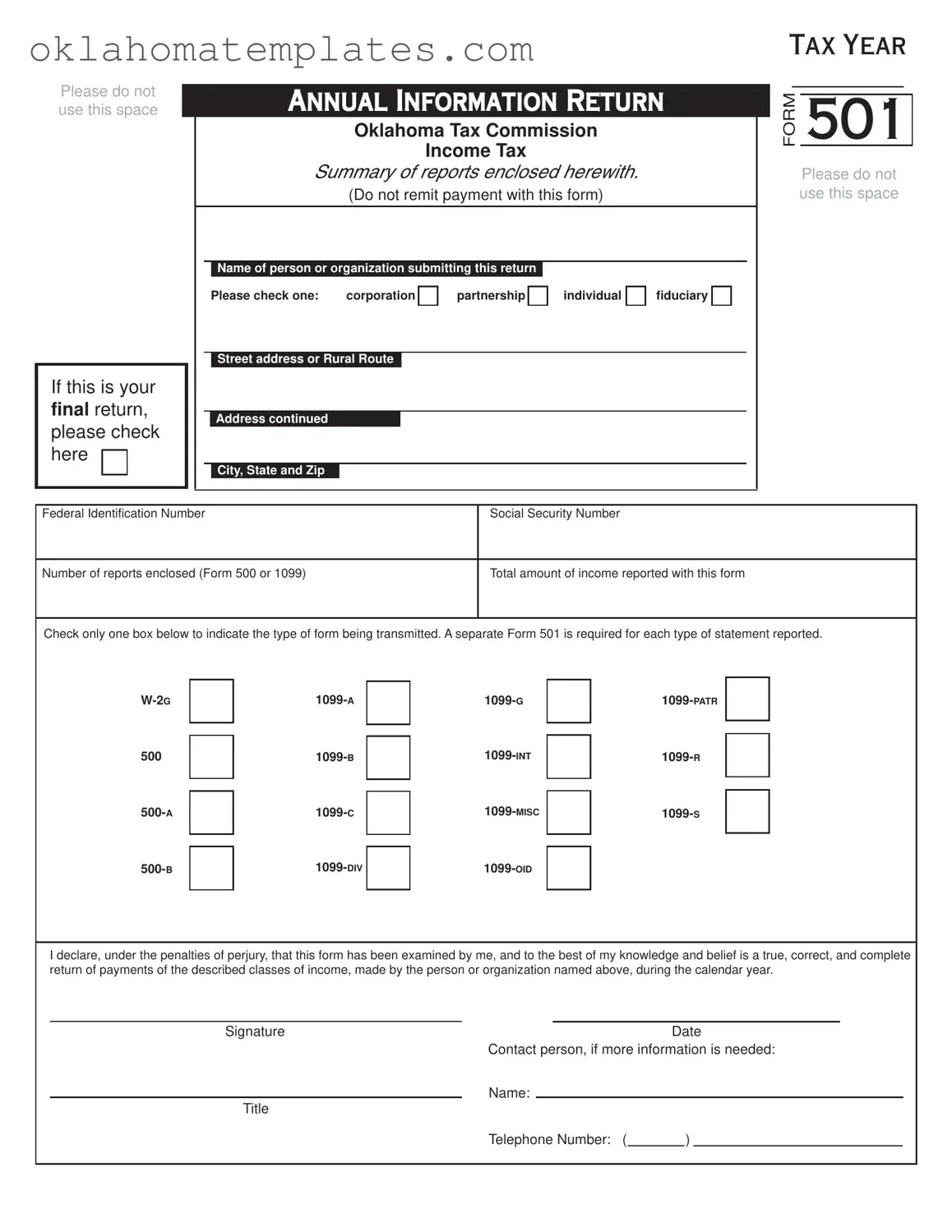

Preview - Oklahoma 501 Form

Please do not use this space

If this is your final return, please check here

ANNUAL INFORMATION RETURN

Oklahoma Tax Commission

Income Tax

Summary of reports enclosed herewith.

(Do not remit payment with this form)

Name of person or organization submitting this return |

|

|

||

Please check one: |

corporation |

partnership |

individual |

fiduciary |

Street address or Rural Route

Address continued

City, State and Zip

TAX YEAR

________

FORM 501

Please do not use this space

Federal Identification Number |

Social Security Number |

|

|

Number of reports enclosed (Form 500 or 1099) |

Total amount of income reported with this form |

|

|

Check only one box below to indicate the type of form being transmitted. A separate Form 501 is required for each type of statement reported.

|

|

|

||||

500 |

|

|

|

|

||

|

|

|

||||

|

|

|

||||

|

|

|

||||

|

|

|

||||

|

|

|

||||

|

|

|

|

|||

|

|

|

|

|||

|

|

|

|

|||

|

|

|

|

|

|

|

I declare, under the penalties of perjury, that this form has been examined by me, and to the best of my knowledge and belief is a true, correct, and complete return of payments of the described classes of income, made by the person or organization named above, during the calendar year.

Signature |

Date |

||||

|

Contact person, if more information is needed: |

||||

|

Name: |

|

|

|

|

Title |

|

|

|

||

|

Telephone Number: ( |

|

) |

|

|

FORM 501 INSTRUCTIONS

WHO SHALL REPORT...

All payors, including but not limited to churches, charitable organizations, labor unions, lodges, fraternities, sororities, school districts, state, county and municipal departments, cooperatives and any other tax exempt organization, shall report these payments.

DUE DATES...

This return together with the reports enclosed must be forwarded so as to reach the Oklahoma Tax Commission before February 28 of the succeeding calendar year except where indicated below.

•Every remitter, required to withhold income tax from royalty payments made to nonresident royalty owners, shall furnish this return together with either Forms

•Every

PAYMENTS TO BE REPORTED WHEN PAID TO RESIDENTS...

All persons (individuals, trusts, estates, corporations and partnerships) acting as payor, and including lessees, mortgagors of real and personal property, employers, officers and employees of the state or any political subdivision thereof, should report the following payments when these payments amount to $750 or more in the calendar year: interest, rent, dividends, annuities, gambling winnings, or other fixed or determinable or periodical gains, profits or income.

PRODUCTION PAYMENT RULES (RESIDENT • NONRESIDENT)...

The Oklahoma Tax Commission requires the reporting of “production payments” made to individuals, corporations, partnerships, trusts or estates whether made to a resident or nonresident. For purposes of Title 68 O.S. 2369, production payments means payments of proceeds generated from mineral interests in this state, including, but not limited to, a lease bonus, delay rental, royalty and working interest payment, and overriding royalty interest payment. Income from real property should be reported only when the property is located within Oklahoma, whether the recipient is a resident or nonresident. Amounts to report: $750 or more except $10 or more for royalties. However, all payments with Oklahoma withholding must be reported. State code “OK” must be entered in box 17 of form

DIVIDEND OR INTEREST PAYMENTS...

Corporations paying to individuals interest on bonds, mortgages, deeds of trusts and other similar obligations or dividend payments, should report these when they exceed $100; other persons (individuals, trusts, estates and partnerships) should report interest payments of $750 or more, when paid to an individual. Brokers or agents in stocks, bonds, and security or stock transactions will report, on Form 500, the total amount of commodity or security sales or the total market value of the securities exchanged for the customer, when they were $25,000 or more in the calendar year. This includes banks which handle orders for depositors or custodian accounts.

NONRESIDENTS...

Persons making payments to nonresident individuals, partnerships, trusts, corporations or estates of fixed or determinable income, from property owned, business or trade carried on in Oklahoma or gambling winnings won in Oklahoma, totaling $750 or more in the calendar year should report such payments. Also see production payment rules for nonresidents.

PROFESSIONAL PAYMENTS...

Persons making payments to professional individuals should report them when they amount to $750 or more and are made to an Oklahoma resident or to a nonresident providing professional services within the State of Oklahoma.

Oklahoma requires withholding from distributions made to nonresident members (partners, members, shareholders or beneficiaries) of

GENERAL INFORMATION...

The foregoing instructions are in conformity with the provisions of the Oklahoma statutes, requiring information returns to be filed in accordance with rules and regulations prescribed and adopted by the Tax Commission. The Oklahoma Tax Commission is not required to notify taxpayers of changes in any state tax law.

MAILING ADDRESS...

Please forward this return and accompanying reports to: Oklahoma Tax Commission, 2501 North Lincoln Blvd., Oklahoma City, Oklahoma

FAQ

What is the Oklahoma 501 form?

The Oklahoma 501 form is an Annual Information Return used to report certain payments made by individuals or organizations to the Oklahoma Tax Commission. This form is essential for documenting various types of income, including wages, dividends, and royalties, and must be submitted along with specific reports such as Forms 1099 or Form 500.

Who is required to file the Oklahoma 501 form?

All payors are required to report payments, including churches, charitable organizations, labor unions, school districts, and other tax-exempt entities. If you are making payments of $750 or more in a calendar year, you must file this form, regardless of your organization type.

When is the deadline for submitting the Oklahoma 501 form?

The form must be submitted to the Oklahoma Tax Commission by February 28 of the year following the tax year, unless specific exceptions apply. For example, payments made to nonresident royalty owners must be reported by January 31.

What types of payments must be reported on the Oklahoma 501 form?

Payments that amount to $750 or more must be reported. This includes interest, rent, dividends, annuities, gambling winnings, and other fixed or determinable gains. For royalties, the reporting threshold is $10.

What if I am reporting payments to nonresidents?

Payments made to nonresident individuals or entities must also be reported if they total $750 or more within the calendar year. This includes income generated from property owned or business activities conducted in Oklahoma, as well as gambling winnings.

Can I submit multiple types of reports with one Oklahoma 501 form?

No, a separate Oklahoma 501 form is required for each type of statement being reported. Ensure that you check the appropriate box to indicate the type of form you are transmitting.

What is the significance of the declaration statement on the form?

The declaration statement is a legal affirmation that the information provided is accurate and complete. By signing, the submitter acknowledges the penalties for perjury if the information is found to be false.

What should I do if I need assistance while completing the form?

If you have questions or need further information while completing the Oklahoma 501 form, you can contact the designated contact person listed on the form. Be sure to provide your name, title, and telephone number for any follow-up inquiries.

Where should I send the completed Oklahoma 501 form?

All completed forms and accompanying reports should be mailed to the Oklahoma Tax Commission at 2501 North Lincoln Blvd., Oklahoma City, Oklahoma 73194-0009. Ensure that you send it well before the deadline to avoid any penalties.

Is payment required when submitting the Oklahoma 501 form?

No payment should be remitted with the Oklahoma 501 form. This form is strictly for reporting purposes and does not require any payment to be included.

Documents used along the form

The Oklahoma 501 form is an important document for reporting various types of income to the Oklahoma Tax Commission. When submitting this form, you may also need to use other related forms and documents. Here’s a list of commonly used forms that often accompany the Oklahoma 501 form, along with a brief description of each.

- Form 500: This form is used to report the total amount of payments made to individuals or entities, typically for services rendered or goods provided. It is essential for payors who need to report income distributions.

- Form 1099-MISC: This form is utilized to report miscellaneous income payments made to non-employees. It is often used for freelancers, contractors, and other service providers.

- Form 1099-INT: This document reports interest income earned by individuals. Banks and other financial institutions typically issue this form to their customers.

- Form 1099-DIV: This form is used to report dividends and distributions paid to shareholders. Companies must provide this form to investors who receive dividend payments.

- Form 1099-R: This form reports distributions from retirement accounts, pensions, and annuities. It is crucial for individuals who withdraw funds from these accounts.

- Form 1099-B: This form is used to report proceeds from broker and barter exchange transactions. It is essential for individuals involved in buying and selling securities.

- Form 1099-C: This document is used to report cancellation of debt. Lenders must provide this form when they forgive a debt of $600 or more.

- Form 1099-S: This form reports proceeds from the sale of real estate. It is important for individuals involved in real estate transactions.

- Medical Power of Attorney: This form allows individuals to designate someone to make healthcare decisions on their behalf if they are unable to do so. It’s crucial for safeguarding your medical preferences, and you can find more information at arizonapdfforms.com/medical-power-of-attorney/.

- Form 500-A: This form is used specifically for reporting payments made to nonresident royalty owners. It is essential for those making royalty payments.

- Form 500-B: This form is required for pass-through entities to report income distributions made to nonresident members. It ensures compliance with withholding requirements.

Using the appropriate forms alongside the Oklahoma 501 form helps ensure compliance with state tax regulations. Each of these forms plays a vital role in accurately reporting income and fulfilling tax obligations. Be sure to review the requirements for each form to avoid any potential issues with the Oklahoma Tax Commission.

Guide to Using Oklahoma 501

Filling out the Oklahoma 501 form requires careful attention to detail. This form is used to report certain payments made during the tax year. Once completed, the form must be submitted to the Oklahoma Tax Commission along with any necessary accompanying reports. Below are the steps to successfully fill out the form.

- Obtain the Form: Download the Oklahoma 501 form from the Oklahoma Tax Commission website or obtain a physical copy.

- Check the Box: If this is your final return, check the designated box at the top of the form.

- Fill in Your Information: Enter the name of the person or organization submitting the return. Specify whether you are a corporation, partnership, individual, or fiduciary.

- Provide Your Address: Fill in your street address or rural route, followed by the city, state, and zip code.

- Indicate the Tax Year: Write the tax year for which you are filing the form.

- Enter Identification Numbers: Provide your Federal Identification Number or Social Security Number as applicable.

- Report Enclosed Documents: Indicate the number of reports you are enclosing, such as Form 500 or 1099.

- State Total Income: Enter the total amount of income reported with this form.

- Select Form Type: Check only one box to indicate the type of form being transmitted. Remember that a separate Form 501 is required for each type of statement reported.

- Sign and Date: Sign the form and enter the date. This declaration confirms that the information provided is accurate to the best of your knowledge.

- Provide Contact Information: If further information is needed, include the name, title, and telephone number of the contact person.

After completing these steps, review the form for any errors or omissions. Ensure that all necessary reports are attached before mailing the form to the Oklahoma Tax Commission at the specified address. Submitting the form accurately and on time is crucial to meet your reporting obligations.