Fill in a Valid Oklahoma 511Tx Template

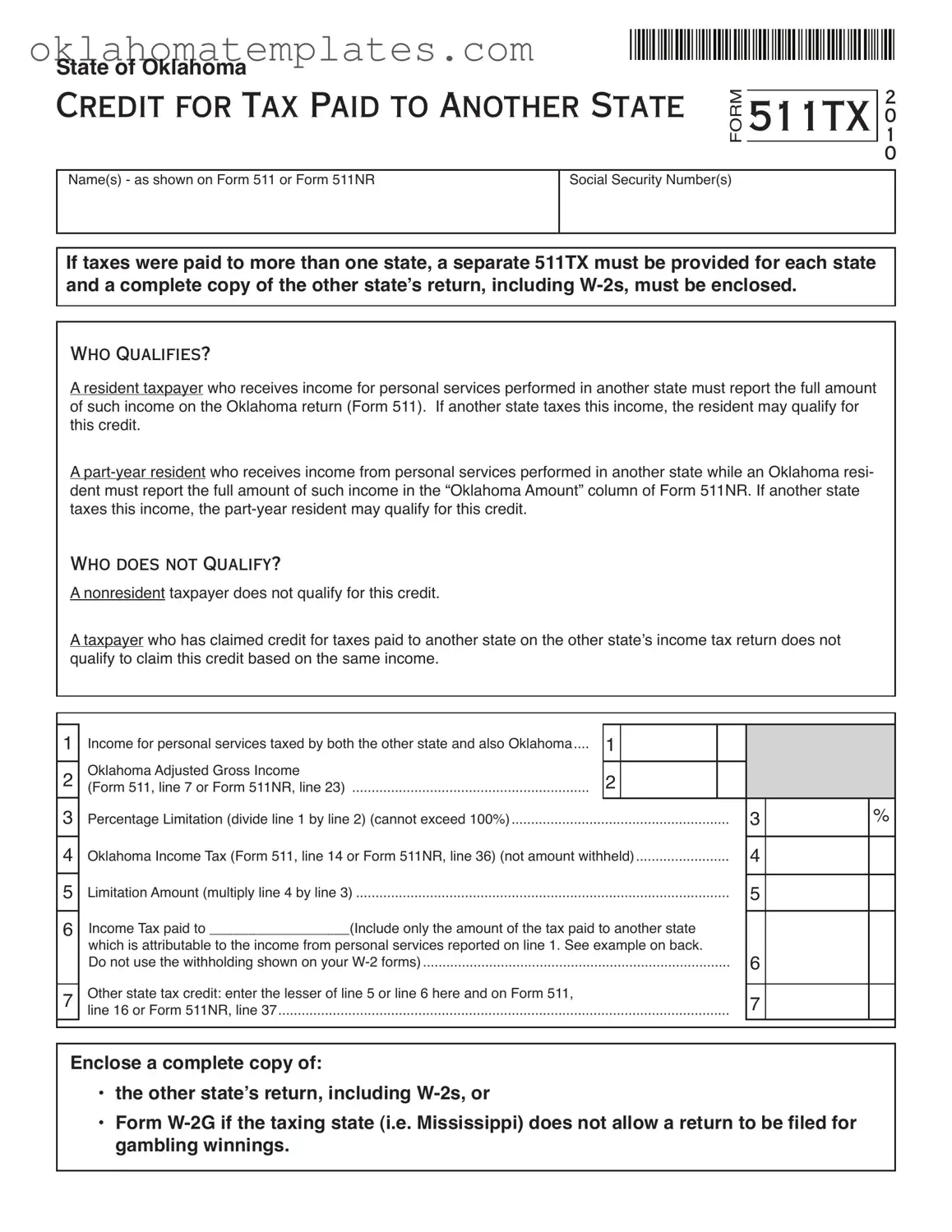

The Oklahoma 511Tx form is an essential document for residents and part-year residents of Oklahoma who earn income from personal services performed in another state. This form allows taxpayers to claim a credit for taxes paid to another state, helping to alleviate the burden of double taxation. To qualify, individuals must report their full income from these services on their Oklahoma tax return, specifically on Form 511 or Form 511NR, depending on their residency status. If taxes were paid to more than one state, separate 511Tx forms must be submitted for each state, along with a complete copy of the other state's tax return and any relevant W-2 forms. However, it’s important to note that nonresidents do not qualify for this credit, nor can taxpayers claim it if they have already received credit on their other state's return for the same income. The form includes specific lines to calculate the amount of income taxed by both Oklahoma and the other state, as well as the corresponding tax paid. By following the guidelines laid out in the form, taxpayers can ensure they receive the appropriate credit, reducing their overall tax liability while complying with Oklahoma tax laws.

Document Properties

| Fact Name | Description |

|---|---|

| Purpose | The Oklahoma 511TX form is used to claim a credit for taxes paid to another state on income earned from personal services. |

| Eligibility | Resident and part-year resident taxpayers who earn income in another state may qualify for this credit. |

| Non-Eligibility | Nonresident taxpayers and those who have already claimed a credit on another state's return do not qualify. |

| Filing Requirement | A separate 511TX form is required for each state where taxes were paid, along with copies of the other state's tax return and W-2s. |

| Governing Law | The form is governed by Title 68 O.S. Section 2357(B)(1) and Rule 710:50-15-72. |

| Income Reporting | Taxpayers must report the full amount of income from personal services on their Oklahoma return. |

| Calculation Method | The credit is calculated based on the proportion of income taxed by both Oklahoma and the other state. |

| Tax Attribution | Only the tax paid to another state that is attributable to the income reported on line 1 should be included. |

| Gambling Winnings | Gambling winnings are considered income from personal services for the purposes of this credit. |

| Documentation | Complete copies of the other state’s return, including W-2s, must be enclosed with the Oklahoma return. |

Common mistakes

-

Incomplete Documentation: One common mistake is failing to include a complete copy of the other state's tax return along with all W-2 forms. This documentation is crucial, as it supports the claim for the credit. Without it, the form may be rejected or delayed.

-

Incorrect Income Reporting: Taxpayers often misreport their income by including amounts that were not taxed by both Oklahoma and the other state. Only the income from personal services that is taxed by both states should be included on Line 1. Misunderstanding this can lead to inaccuracies in the credit calculation.

-

Using Withholding Amounts: Another frequent error is entering the amount of tax withheld from W-2 forms instead of the actual tax paid to the other state. Line 6 specifically requires the tax attributable to the income reported on Line 1, not the withholding amounts.

-

Filing Multiple Forms: Individuals who have income taxed in more than one state may mistakenly believe they can use a single 511TX form for all states. In reality, a separate 511TX must be submitted for each state where taxes were paid, along with the required documentation for each.

Popular PDF Documents

Oklahoma New Hire Reporting - Employers are advised to file the report promptly to avoid accruing interest and penalties.

To ensure a smooth transaction and meet legal requirements, it is advisable to utilize reliable resources when drafting a Texas RV Bill of Sale form. One such resource is UsaLawDocs.com, which provides templates and guidance for creating a comprehensive document that protects the interests of both parties involved in the sale.

Licensed Handyman - All payments should be made out to the Construction Industries Board at their official address in Oklahoma City.

Do You Need Permit to Build Fence - This application collects essential information about the project, including the project name and address.

Misconceptions

Misconceptions about the Oklahoma 511Tx form can lead to confusion and potentially costly mistakes. Here are five common misunderstandings:

- Only residents can claim the credit. Many people believe that only full residents of Oklahoma can claim the credit for taxes paid to another state. However, part-year residents who earned income while living in Oklahoma and were taxed by another state may also qualify.

- All income is eligible for the credit. It’s a common misconception that any income earned in another state qualifies for the credit. In reality, only income from personal services that has been taxed by both Oklahoma and the other state is eligible for this credit.

- You don’t need to submit additional documentation. Some taxpayers think they can simply fill out the 511Tx form without any supporting documents. In fact, it is necessary to enclose a complete copy of the other state’s tax return and all relevant W-2 forms when submitting the Oklahoma return.

- Withholding amounts can be claimed. A frequent misunderstanding is that taxpayers can use the withholding amounts shown on their W-2 forms when calculating the credit. This is incorrect; only the actual tax paid to the other state based on the income reported is applicable.

- Filing for one state is enough. Many individuals mistakenly believe that if they file a tax return in one state, they do not need to report the income on their Oklahoma return. In truth, all income must be reported on the Oklahoma return, even if it has been taxed by another state.

Preview - Oklahoma 511Tx Form

State of Oklahoma

CREDIT FOR TAX PAID TO

Name(s) - as shown on Form 511 or Form 511NR

|

|

FORM |

511TX |

10 |

ANOTHER STATE |

|

|

2 |

|

|

|

|

||

|

|

|

0 |

|

|

Social Security Number(s) |

|

|

|

|

|

|

||

|

|

|

|

|

If taxes were paid to more than one state, a separate 511TX must be provided for each state and a complete copy of the other state’s return, including

WHO QUALIFIES?

A resident taxpayer who receives income for personal services performed in another state must report the full amount of such income on the Oklahoma return (Form 511). If another state taxes this income, the resident may qualify for this credit.

A

WHO DOES NOT QUALIFY?

A nonresident taxpayer does not qualify for this credit.

A taxpayer who has claimed credit for taxes paid to another state on the other state’s income tax return does not qualify to claim this credit based on the same income.

|

|

|

|

|

|

|

|

1 |

Income for personal services taxed by both the other state and also Oklahoma.... |

1 |

|

|

|

|

|

|

Oklahoma Adjusted Gross Income |

|

|

|

|

|

|

2 |

2 |

|

|

|

|

|

|

(Form 511, line 7 or Form 511NR, line 23) |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

3 |

Percentage Limitation (divide line 1 by line 2) (cannot exceed 100%) |

|

|

|

3 |

|

% |

|

|

|

|

|

|||

4 |

Oklahoma Income Tax (Form 511, line 14 or Form 511NR, line 36) (not amount withheld) |

4 |

|

|

|||

|

|

|

|

|

|

|

|

5 |

Limitation Amount (multiply line 4 by line 3) |

|

|

|

5 |

|

|

|

|

|

|

|

|||

6 |

Income Tax paid to __________________(Include only the amount of the tax paid to another state |

|

|

|

|||

|

which is attributable to the income from personal services reported on line 1. See example on back. |

|

|

|

|||

|

Do not use the withholding shown on your |

|

|

|

6 |

|

|

|

Other state tax credit: enter the lesser of line 5 or line 6 here and on Form 511, |

|

|

|

|

|

|

7 |

|

|

|

7 |

|

|

|

line 16 or Form 511NR, line 37 |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Enclose a complete copy of:

•the other state’s return, including

•Form

FORM 511TX - CREDIT FOR TAX PAID TO ANOTHER STATE

TITLE 68 O.S. SECTION 2357(B)(1) AND RULE

INSTRUCTIONS

This schedule, a complete copy of the other state’s tax return and copies of all

Line 1

Include only the amount of wages, salaries, commissions and other pay for personal services which is being taxed by Oklahoma and also the other state. Gambling winnings are considered income from personal services for purposes of this credit.

Example 1. John is an Oklahoma resident, filing Form 511. He worked and owned rental property in an- other state. The other state’s return shows wages of $20,000 and rental income of $10,000. Line 1 would be $20,000, the amount of income from personal services included in his Okla- homa adjusted gross income and taxed by another state.

Example 2. Beth is a

Line 6

Include only the amount of the tax paid to another state which is attributable to the income from personal services reported on line 1. Do not use the withholding shown on your

Example: personal services (from line 1) total income from another state

Xtotal tax paid to another state = tax paid to another state (not withholding tax)

Example 1. Bill is an Oklahoma resident, filing Form 511. The other state’s return shows $5,000 in wages,

$7,000 in rental income from the other state, and $8,000 from the sale of a house located in the other state. The other state’s total tax liability is $546. Since only the $5,000 in wages is income from personal services subject to tax in both states, line 6 would be computed as fol-

lows: |

$5,000 X $546 = $137 |

|

$20,000 |

Example 2. (continued from Line 1, Example 2 above)

The other state taxed all of Beth’s wage income; however, only the portion she earned while an Oklahoma resident was taxed by both states (see line 1). Her other state’s total tax liability was $754. Beth determines the portion of the other state’s tax that is attributable to the por- tion of her wage income which is being taxed in both states as follows:

$22,500 X $754 = $566 $30,000

FAQ

What is the Oklahoma 511Tx form?

The Oklahoma 511Tx form is a tax document used by residents and part-year residents of Oklahoma who have earned income from personal services in another state and have paid taxes on that income to that state. This form allows taxpayers to claim a credit for the taxes paid to another state, helping to avoid double taxation on the same income. It is essential to file this form along with your Oklahoma income tax return, either Form 511 or Form 511NR, depending on your residency status.

Who qualifies to use the 511Tx form?

To qualify for the Oklahoma 511Tx form, you must be a resident taxpayer or a part-year resident who has earned income from personal services performed in another state. This income must be reported on your Oklahoma tax return. If the other state taxes this income, you may be eligible for a credit. Remember, if you are a nonresident taxpayer, you do not qualify for this credit.

What information do I need to provide on the 511Tx form?

When filling out the 511Tx form, you need to include your Social Security Number, the amount of income from personal services that has been taxed by both Oklahoma and the other state, and the amount of tax paid to the other state. Additionally, you must enclose a complete copy of the other state’s tax return, including all W-2 forms. If the other state does not allow a return for certain types of income, such as gambling winnings, include Form W-2G instead.

What happens if I paid taxes to more than one state?

If you have paid taxes to more than one state, you must complete a separate 511Tx form for each state. Each form should be accompanied by a complete copy of the respective state’s tax return and W-2 forms. This ensures that you accurately report and claim credits for taxes paid to multiple jurisdictions.

Can I claim a credit for taxes paid to another state if I have already claimed it on that state's tax return?

No, you cannot claim a credit on the Oklahoma 511Tx form for taxes you have already claimed on the other state's tax return. If you have received a credit for the same income in the other state, you are ineligible to claim it again on your Oklahoma return. This rule helps to prevent double dipping and ensures fairness in the tax system.

How do I calculate the amount of credit I can claim?

To calculate the credit amount, you will need to follow a few steps. First, determine the income from personal services that was taxed by both states. Then, find your Oklahoma adjusted gross income. Divide the income from personal services by your adjusted gross income to find the percentage limitation, which cannot exceed 100%. Multiply this percentage by your Oklahoma income tax amount to find your limitation amount. Finally, compare this amount to the actual tax paid to the other state and enter the lesser of the two on your 511Tx form.

What should I do if I need assistance with the 511Tx form?

If you find yourself needing assistance with the Oklahoma 511Tx form, consider reaching out to a tax professional or an accountant. They can provide valuable guidance tailored to your specific situation. Additionally, you can consult the Oklahoma Tax Commission's website for more resources and information regarding the form and the credit process. Taking these steps can help ensure that your tax filings are accurate and compliant.

Documents used along the form

The Oklahoma 511Tx form is used by residents and part-year residents to claim a credit for taxes paid to another state. This form is often accompanied by several other documents that provide necessary information for accurate tax filing. Below is a list of common forms and documents that may be needed alongside the 511Tx.

- Oklahoma Form 511: This is the primary income tax return for Oklahoma residents. It reports total income and calculates the state tax owed.

- Oklahoma Form 511NR: This form is for part-year residents. It allows individuals to report income earned while living in Oklahoma and to determine the tax owed for that period.

- Other State Tax Return: A complete copy of the tax return from the other state where income was earned must be provided. This shows the amount of tax paid to that state.

- W-2 Forms: These forms report wages earned and taxes withheld. Copies of W-2s from both Oklahoma and the other state must be included to verify income and tax payments.

- Form W-2G: This form is used for reporting gambling winnings. If the other state does not allow a tax return for such income, this form must be submitted instead.

- Income Statements: Additional documentation that shows other sources of income, such as 1099 forms, may be required to ensure all income is reported accurately.

- Tax Payment Receipts: Proof of payment for taxes paid to the other state can help substantiate the credit claimed on the 511Tx form.

- Missouri Power of Attorney Form: For individuals seeking to delegate authority, our comprehensive Missouri Power of Attorney guidelines provide essential insights into the form's necessity and use.

- Schedule C or Schedule E: If the taxpayer has business income or rental income, these schedules may be needed to report additional income sources properly.

Gathering these documents is essential for a smooth filing process. Each item plays a role in ensuring that the taxpayer receives the appropriate credit for taxes paid to another state, ultimately affecting their overall tax liability.

Guide to Using Oklahoma 511Tx

Filling out the Oklahoma 511Tx form requires careful attention to detail. This form is used to claim a credit for taxes paid to another state. To ensure accuracy, gather all necessary documents, including your W-2 forms and the other state's tax return. Follow the steps below to complete the form correctly.

- Enter your name(s) as shown on Form 511 or Form 511NR.

- Provide your Social Security Number(s).

- If you paid taxes to more than one state, prepare a separate 511Tx for each state.

- On line 1, report the income for personal services taxed by both Oklahoma and the other state.

- On line 2, enter your Oklahoma Adjusted Gross Income. This is found on Form 511, line 7 or Form 511NR, line 23.

- Calculate the Percentage Limitation on line 3 by dividing line 1 by line 2. This percentage cannot exceed 100%.

- On line 4, enter your Oklahoma Income Tax from Form 511, line 14 or Form 511NR, line 36. Do not include the amount withheld.

- Multiply the amount on line 4 by the percentage from line 3 to find the Limitation Amount on line 5.

- On line 6, enter the amount of income tax paid to the other state that is attributable to the income reported on line 1. Do not use withholding amounts from your W-2 forms.

- On line 7, write the lesser of line 5 or line 6. This is the amount to enter on Form 511, line 16 or Form 511NR, line 37.

- Attach a complete copy of the other state’s tax return, including W-2s, or Form W-2G if applicable.