Fill in a Valid Oklahoma 511X Template

The Oklahoma 511X form serves as a crucial tool for individuals seeking to amend their resident income tax returns for tax years prior to 2006. This form is specifically designed for residents who need to correct mistakes or update information on their original returns. It is important to note that part-year and non-residents must use a different form, the 511NR. The 511X requires taxpayers to provide their Social Security numbers, filing status, and details about their income and deductions. Additionally, if a taxpayer has amended their federal return, they must include supporting documents, such as IRS Form 1040X, to ensure proper processing. The form also allows for the declaration of exemptions and credits, which can significantly impact the final tax liability. Taxpayers must be mindful of deadlines, as amended returns must generally be filed within three years of the original due date. Understanding the requirements and instructions for the 511X can help individuals navigate the amendment process more effectively, ultimately leading to a smoother experience with the Oklahoma Tax Commission.

Document Properties

| Fact Name | Description |

|---|---|

| Purpose | The Oklahoma 511X form is used to amend a previously filed resident individual income tax return for tax years 2005 and prior. |

| Filing Requirement | Part-year and non-residents must use Form 511NR to amend their returns, not the 511X form. |

| Deadline for Amending | Generally, to claim a refund, the amended return must be filed within three years from the date tax, penalty, and interest were paid. |

| IRS Confirmation | If you amend your Federal return, it is advisable to obtain IRS confirmation before filing the Oklahoma 511X to avoid processing delays. |

| Governing Law | The use of Form 511X is governed by the Oklahoma Statutes Title 68, Section 2355.1, which outlines the requirements for amending tax returns. |

Common mistakes

-

Incorrect Form Version: Using an outdated version of Form 511X can lead to processing delays. Ensure you are using the correct version for the tax year you are amending, specifically for Tax Year 2005 and prior.

-

Missing Social Security Numbers: Failing to include the Social Security Number for both the taxpayer and spouse (if applicable) can result in rejection of the form. Always double-check this information.

-

Improper Filing Status: Selecting a filing status that differs from the original federal return can cause complications. Make sure the filing status on Form 511X matches what was reported on your federal return.

-

Neglecting Required Documents: Not enclosing necessary documents, such as a copy of the amended federal return (Form 1040X) or proof of IRS approval, may delay processing. Always include these documents when submitting your form.

-

Incorrect Calculations: Errors in calculating income, deductions, or credits can lead to incorrect tax liabilities. Review all calculations carefully to ensure accuracy.

-

Failure to Sign: Forgetting to sign the form is a common mistake. Both the taxpayer and spouse (if filing jointly) must sign and date the form for it to be valid.

Popular PDF Documents

Oklahoma Efs 1 - Care should be taken to ensure all codes and descriptions match state requirements.

Oklahoma Food Tax - The form is straightforward, but careful attention to detail is necessary for eligibility.

The Arizona Homeschool Letter of Intent is a document that parents must submit to formally notify the state of their decision to homeschool their children. This form serves as an essential step in the homeschooling process, ensuring compliance with Arizona's educational regulations. By completing this letter, parents take an important step in establishing their homeschooling journey, and they can find more information at arizonapdfforms.com/homeschool-letter-of-intent.

Do You Need Permit to Build Fence - Filing the application properly is critical to ensure compliance and avoid penalties.

Misconceptions

Misconception 1: The Oklahoma 511X form can be used for any tax year.

This is incorrect. The 511X form is specifically for Tax Year 2005 and prior. If you need to amend a return for Tax Year 2006 or later, you must use the updated version of the form.

Misconception 2: You can file the 511X form without any supporting documents.

In fact, it is essential to enclose supporting documents, such as the amended Federal return (Form 1040X) and proof of any changes. Failing to do so may delay your refund.

Misconception 3: Only residents of Oklahoma can use the 511X form.

While the form is for residents, part-year and non-residents must use a different form, specifically the 511NR, to amend their returns.

Misconception 4: You can amend your Oklahoma return at any time.

There is a time limit. Generally, you must file your amended return within three years from the date you paid the tax, penalty, and interest. For Federal changes, the time frame is one year.

Misconception 5: You only need to submit the 511X form to amend your return.

In addition to the 511X, you must provide copies of relevant documents that support your changes. This includes IRS forms and any additional schedules related to the adjustments.

Misconception 6: You can combine amendments for multiple years on a single 511X form.

This is not allowed. You must file a separate 511X form for each tax year you are amending. Each year requires its own documentation and processing.

Misconception 7: You do not need to notify the IRS before amending your Oklahoma return.

If your Federal return has changed, it is advisable to obtain confirmation from the IRS before filing the 511X. This can help avoid delays in processing your Oklahoma amendment.

Misconception 8: Filing the 511X will automatically result in a refund.

A refund is not guaranteed. The amount you receive depends on the adjustments made and whether you have overpaid your taxes. If you owe additional tax, you will need to pay that amount.

Misconception 9: You can use the 511X form to amend any errors on your original return.

While the 511X is for amending returns, it is only appropriate for errors related to the Oklahoma state tax. If you need to correct Federal tax errors, you should address those separately with the IRS.

Misconception 10: You can file your amended return electronically.

Currently, the 511X form must be filed by mail. Ensure that you send it to the correct address along with all required documentation for processing.

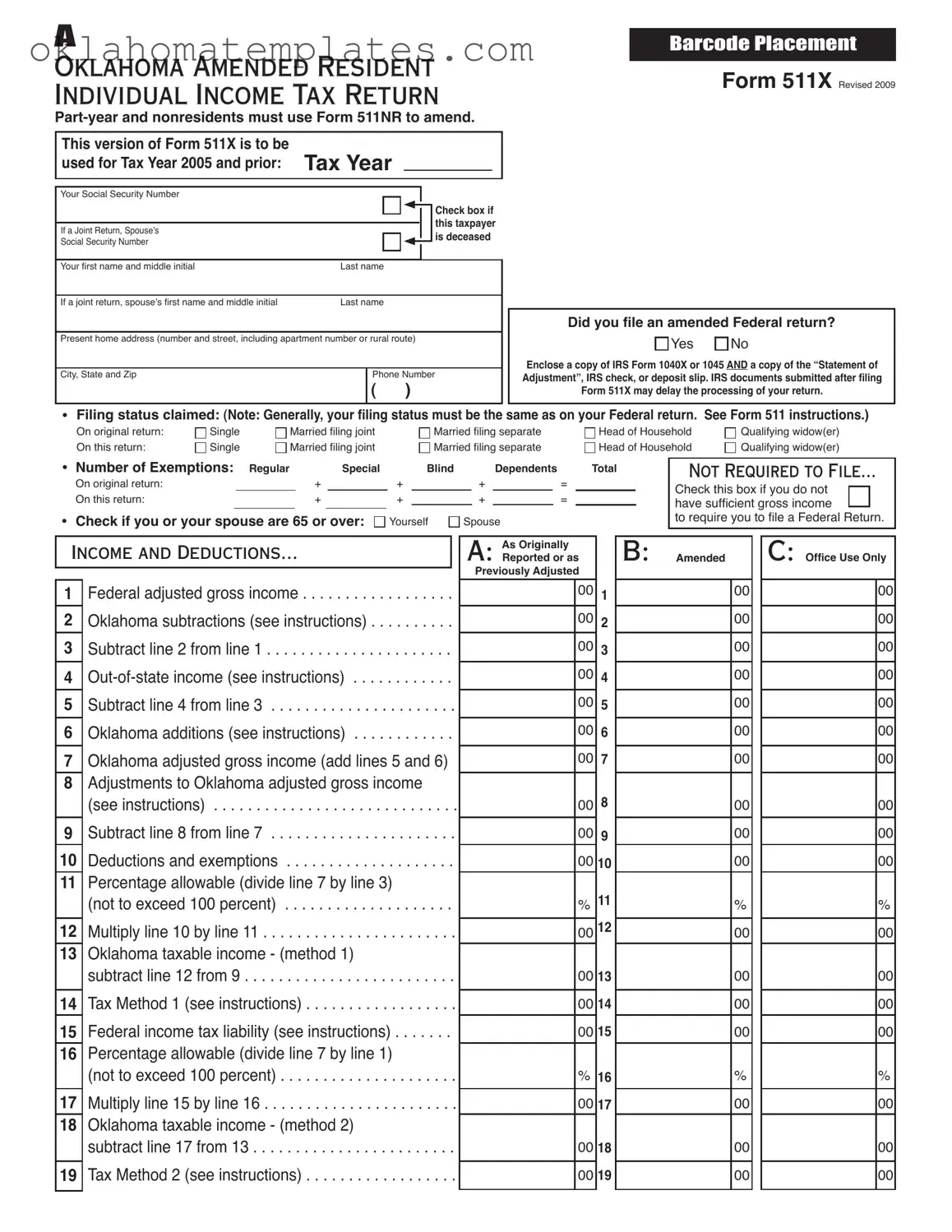

Preview - Oklahoma 511X Form

A

Oklahoma Amended Resident Individual Income Tax Return

BARCODE PLACEMENT

Form 511X Revised 2009

This version of Form 511X is to be

used for Tax Year 2005 and prior: Tax Year

Your Social Security Number |

|

|

|

|

|

|

Check box if |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

this taxpayer |

If a Joint Return, Spouse’s |

|

|

|

|

|

||

Social Security Number |

|

|

|

|

|

|

is deceased |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Your irst name and middle initial |

Last name |

|

|

|

|

||

|

|

|

|

|

|

|

|

If a joint return, spouse’s irst name and middle initial |

Last name |

|

|

|

|

||

|

|

|

|

|

|

|

|

Present home address (number and street, including apartment number or rural route) |

|||||||

|

|

|

|

|

|

|

|

City, State and Zip |

|

Phone Number |

|||||

|

|

( |

|

) |

|

|

|

Did you ile an amended Federal return?

Yes |

No |

Enclose a copy of IRS Form 1040X or 1045 AND a copy of the “Statement of Adjustment”, IRS check, or deposit slip. IRS documents submitted after iling Form 511X may delay the processing of your return.

•Filing status claimed: (Note: Generally, your iling status must be the same as on your Federal return. See Form 511 instructions.)

|

On original return: |

Single |

Married iling joint |

|

Married iling separate |

|

||||||||||

|

On this return: |

Single |

Married iling joint |

|

Married iling separate |

|

||||||||||

• |

Number of Exemptions: Regular |

|

|

|

|

Special |

|

Blind |

|

|

Dependents |

|

||||

|

On original return: |

|

|

|

|

+ |

|

|

+ |

|

|

+ |

|

|

= |

|

|

On this return: |

|

|

|

+ |

|

|

+ |

|

+ |

|

|

= |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

Check if you or your spouse are 65 or over: |

Yourself |

Spouse |

|

||||||||||||

Head of Household |

Qualifying widow(er) |

Head of Household |

Qualifying widow(er) |

Total |

|

|

Not Required to File... |

|

|

|

Check this box if you do not |

|

|||

|

|

|

have suficient gross income |

|

|

||

|

|

|

to require you to ile a Federal Return. |

Income and Deductions...

1 |

.Federal adjusted gross income |

2 |

.Oklahoma subtractions (see instructions) |

3 |

Subtract line 2 from line 1 |

4 |

|

5 |

Subtract line 4 from line 3 |

6 |

.Oklahoma additions (see instructions) |

7 |

Oklahoma adjusted gross income (add lines 5 and 6) |

8 |

Adjustments to Oklahoma adjusted gross income |

|

(see instructions) |

9 |

.Subtract line 8 from line 7 |

10 |

Deductions and exemptions |

11 |

Percentage allowable (divide line 7 by line 3) |

|

(not to exceed 100 percent) |

12 |

.Multiply line 10 by line 11 |

13 |

Oklahoma taxable income - (method 1) |

|

subtract line 12 from 9 |

14 |

.Tax Method 1 (see instructions) |

15 |

Federal income tax liability (see instructions) |

16 |

Percentage allowable (divide line 7 by line 1) |

|

(not to exceed 100 percent) |

17 |

.Multiply line 15 by line 16 |

18 |

Oklahoma taxable income - (method 2) |

|

subtract line 17 from 13 |

19 |

.Tax Method 2 (see instructions) |

A: As Originally

Reported or as

Previously Adjusted

00 1

00 2

00 3

00 4

00 5

00 6

00 7

00 8

00 9

00 10

% 11 00 12

00 13

00 14

00 15

% 16

00 17

00 18

00 19

B: Amended

00

00

00

00

00

00

00

00

00

00

%

00

00

00

00

%

00

00

00

C: Ofice Use Only

00

00

00

00

00

00

00

00

00

00

%

00

00

00

00

%

00

00

00

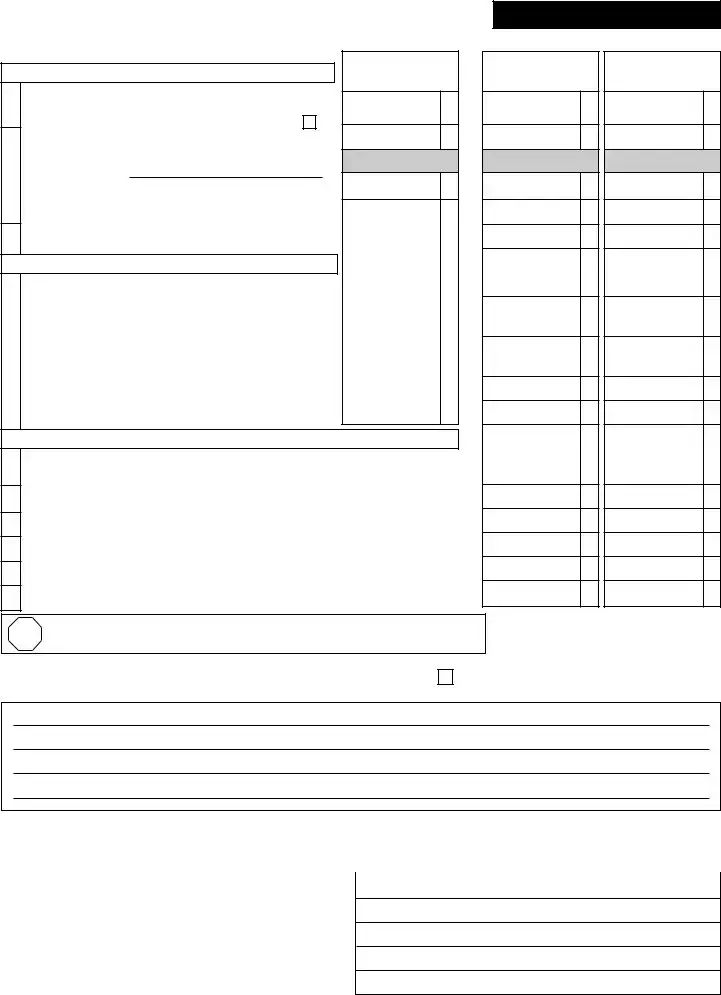

Form 511X (A) - Page 2

BARCODE PLACEMENT

Tax Liability...

20Income Tax: Enter lesser of line 14 or 19 (from front of form)

If using Farm Income Averaging, enter Form 573, line 42 and check here

21A. Oklahoma

B.Subtotal: Subtract line 21A from line 20 (not less than zero)

C.Use tax (beginning with Tax Year 2003) . . . . . . . .

22Total tax - (add lines 21B and 21C) . . . . . . . . . . . . .

Payments...

23 |

Oklahoma income tax withheld |

|

24 |

Oklahoma estimated tax paid plus amount paid |

|

|

|

with extension |

25 |

Amount paid with original return plus additional paid |

|

|

|

after it was iled |

26 |

.Refundable credits (see instructions) |

|

27 |

Total of lines 23 through 26 |

|

Refund or Amount You Owe...

A: As Originally

Reported or as

Previously Adjusted

00 20

00 21A

00 21B

00 21C |

|

00 |

22 |

|

|

00 |

23 |

00 |

24 |

00 |

25 |

00 |

26 |

00 |

27 |

B: Amended

00

00

00

00

00

00

00

00

00

00

C: Ofice Use Only

00

00

00

00

00

00

00

00

00

00

28Overpayment, if any, as shown on original return or as previously adjusted

|

by Oklahoma (see instructions) |

. . . . . . . . . 28 |

|

|

29 |

29 |

Subtract line 28 from line 27 |

. . . . . . . . . |

30 |

Refund: If line 29 is more than line 22 enter difference |

. . . . . . . . . 30 |

|

|

31 |

31 |

Tax liability: If line 22 is more than line 29 enter difference . . . . |

. . . . . . . . . |

32Interest: 1.25% per month from _______________ to ________________ 32

33Total amount due (add lines 31 and 32) please pay in full with this return . 33

00

00

00

00

00

00

00

00

00

00

00

00

STOP |

If you are changing your Oklahoma return due to a change to your |

|

Federal return, enclose proof that the IRS approved the change. |

Explain below or attach a separate schedule, if necessary, explaining the changes to income, deductions, and/or credits: (Enter the line reference number for which you are reporting a change and give the reason for each change in column “B”)

Please check here if the Oklahoma Tax Commission may discuss this return with your tax preparer.

The Oklahoma Tax Commission is not required to give actual notice to taxpayers of changes in any state tax law.

Remit to: Oklahoma Tax Commission, P.O. Box 26800, Oklahoma City, Oklahoma

Under penalties of perjury, I declare that I have iled an original return and that I have examined this return including accompanying schedules and statements, and to the best of my knowledge this amended return is true, correct and complete.

Taxpayer signature |

|

Date |

|

|

|

Spouse’s signature (if iling jointly both must sign) |

Date |

|

|

|

|

Daytime Phone Number (optional) |

|

|

( |

) |

|

|

|

|

Preparer’s signature |

Date |

Preparer’s printed name

Preparer’s Address

Preparer’s ID Number

Phone Number (if box is checked above)

()

Instructions for Form 511X

This form is for residents only.

When to File an Amended Return

Generally, to claim a refund your amended return must be iled within three years from the date tax, penalty and interest was paid. For most taxpayers, the three year period begins on the original due date of the Oklahoma tax return. Estimated tax and withholding are deemed paid on the original due date (excluding extensions).

If your Federal return for any year is changed, an amended Oklahoma return shall be iled within one year. If you amend your Federal return, it is recommended you obtain conirmation the IRS approved your Federal amendment before iling Oklahoma Form 511X. Filing Form 511X without such IRS conirmation may delay the processing of your return, however, this may be necessary to avoid the expiration of the statute of limitation.

File a separate Form 511X for each year you are amending. No amended return may encompass more than one single year.

If you discover you have made an error only on your Oklahoma return we may be able to make the corrections over the phone instead of iling Form 511X. For additional information, call our Taxpayer Assistance Division at (405)

When completing this form, it is recommended you have the Resident Individual Income Tax Instructions booklet (511 Packet) for the tax year you are amending. The packet will provide detailed explanation. If you do not have a copy, one may be downloaded from our website (www.tax.ok.gov) beginning with tax year 1997 or you may order a packet for any tax year by calling our forms request line at (405)

Before You Begin

This version of Form 511X is for Tax Year 2005 and prior years. If you need to amend for Tax Year 2006 or thereafter, visit our website and download the Form 511X for 2006 and thereafter. You may also order the form at (405)

The tax rates did not change during the tax years of 1990 - 1998. The tax rates also remained unchanged for the tax years 1999 - 2001, for tax years 2002 - 2003 and for tax years 2004 - 2005. Thus, if you are amending a 2000 return, you may refer to the tax tables for any year from 1999 - 2001.

All entries in column “B” must be substantiated by an enclosed document or your refund may be delayed. After completing your amended return, see the “When You Are Finished” section of the instructions for a complete list of necessary docu- ments you must enclose with this return.

Any additional forms, necessary to complete this amended return, can be downloaded from our website (www.tax.ok.gov) beginning with tax year 1997 or can be ordered by calling our forms request line at (405)

Select Line Instructions

Column A: Enter the amounts from your original return. However, if you previously amended that return or it was changed by the Oklahoma Tax Commission, enter the adjusted amounts.

Column B: Enter the amended amounts and explain each change on Page 2. If you need more space, attach a statement. Also, attach any schedule or form relating to the change. For any item you do not change, enter the amount from Column A in Column B. All entries in Column B must be substantiated

by an enclosed document or your refund may be delayed. Column C: Do not use. This column is for Oklahoma Tax Commission use only.

1

2

Enter the Federal adjusted gross income. Note: Enclose supporting documents for any adjustments to your Federal adjust- ed gross income.

Enter subtractions to Federal adjusted gross income, such as interest from U.S. government obligations (no IRS interest), retire- ment income, social security beneits and depletion. A complete list of subtractions can be found in the Schedule

4

Enter

spreadsheets.

6

Enter additions to Federal adjusted gross income, such as

8

Enter all adjustments to your Oklahoma adjusted gross income, such as military pay exclusion, political contributions, interest qualifying for exclusion and Indian employment exclusion. A complete list of adjustments can be found in the Schedule

10

Enter the total amount of your deductions and exemptions. Add your “Oklahoma standard deduction or Federal itemized deduc- tions” and your Oklahoma “exemption amounts”.

14The tax rates did not change during the tax years of 1990 - 1998. The tax rates also remained unchanged for tax years 1999 -

and 2001, for tax years 2002 - 2003 and for tax years 2004 - 2005. Thus, if you are amending a 2000 return, you may refer to the tax

19tables for any year from 1999 - 2001.

15

20

21

25

26

28

Enter the Federal income tax liability from your Federal return. Do not include

your Federal return for veriication.

If you have farm income, beginning in tax year 2001, you may elect to igure your tax by averaging your farm income over the previous three years. If you choose this option, you must use Form 573 to compute the tax. Note: Enclose Form 573.

A. Enter all

B. Enter the subtotal.

C. Beginning in tax year 2003, you have the ability to remit “use tax” with your income tax return. Use tax is due on purchases from

Enclose a schedule of payments by amount and date paid. Underpayment interest is based on the tax on the original return. Do not include underpayment interest in your calculations.

Oklahoma refundable credits, such as low income property tax credit (enclose Form

This includes all amounts refunded to you, applied to next year’s estimated tax and donated from your refund (for example, a donation to the Wildlife Diversity Program).

If you originally iled a Form 511, use the amount from the line shown here: |

|

|

|||

2000: line 57 |

2001: line 31 |

2002: line 32 |

2003: line 34 |

2004: line 34 |

2005: line 35 |

30Total amount of overpayment must be refunded. None can be placed in estimated tax for the following year.

32Compute interest on your income tax liability only. Do not compute interest on the portion of your tax liability that represents use tax.

When You are Finished

Enclose a copy of the following support documents, if applicable:

•Form 1040X (Amended Federal Income Tax Return) or Form 1045 (Application for Federal Tentative Return),

•Proof that IRS has approved the claim, such as the statement of adjustment, any correspondence from IRS, or the deposit slip of your Federal refund,

•Revenue Agent Report (RAR), CP2000 or other notiication of an assessment or a change made by the IRS,

•Additional Forms

•Forms, schedules or other documentation to substantiate any of the entries in Column B of Form 511X as indicated in the Select Line Instructions.

Do not enclose any correspondence other than those documents required for your amended return. Do not enclose amendments for different years in the same envelope. Use a separate envelope for each tax year.

Sign your return and mail it, along with all required documents to: Oklahoma Tax Commission, P.O. Box 26800, Oklahoma City, OK

FAQ

What is the purpose of the Oklahoma 511X form?

The Oklahoma 511X form is used to amend a previously filed Oklahoma Resident Individual Income Tax Return. If you need to correct errors or make changes to your original return, this form allows you to do so. However, if you are a part-year resident or a non-resident, you must use Form 511NR instead. It’s important to file this form within the appropriate time frame to ensure you can claim any refunds you may be entitled to.

When should I file the 511X form?

You should file the 511X form if you need to amend your Oklahoma tax return. Generally, you must file it within three years from the date you paid your taxes, penalties, and interest. This period usually starts from the original due date of your return. If you have amended your federal return, you should also file an amended Oklahoma return within one year of the federal change. It’s best to wait until you receive confirmation from the IRS regarding your federal amendment before submitting the 511X, as this can help avoid delays.

What documents do I need to include with my 511X form?

When submitting your 511X form, you must include several supporting documents. These include a copy of your amended federal return (Form 1040X or 1045) and proof that the IRS has approved your changes, such as a statement of adjustment. You may also need to provide additional forms like W-2s or 1099s that were not included with your original return. All entries in the amended section must be supported by relevant documentation to avoid delays in processing.

Can I make changes to my Oklahoma return over the phone?

If you discover an error only on your Oklahoma return, you may be able to correct it by calling the Taxpayer Assistance Division. This option is available in some cases and could save you from having to file the 511X form. For assistance, you can reach them at (405) 521-3160 or toll-free at (800) 522-8165 within Oklahoma.

What if I need to amend multiple tax years?

If you need to amend returns for multiple years, you must file a separate 511X form for each tax year you are amending. Each form should be sent in its own envelope. This helps ensure that each amendment is processed correctly and efficiently. Remember, you cannot include amendments for different years in the same envelope.

Documents used along the form

The Oklahoma 511X form is used to amend a resident individual income tax return. When filing this form, there are several other documents that may be required to ensure proper processing. Below is a list of forms and documents that are often used alongside the Oklahoma 511X form.

- Form 511NR: This form is for part-year and nonresidents who need to amend their Oklahoma tax returns. It's essential for those who do not meet the residency requirements but still have tax obligations in Oklahoma.

- IRS Form 1040X: This is the Amended U.S. Individual Income Tax Return. Taxpayers must include this form when amending their federal return, as it provides the IRS with details on what changes were made.

- Texas Quitclaim Deed: This form is utilized to transfer interest in real property without guaranteeing title validity. For more information, visit UsaLawDocs.com.

- IRS Form 1045: This form is used to apply for a federal tentative refund. It can be filed when a taxpayer wants to expedite their refund due to changes in their tax situation.

- Revenue Agent Report (RAR): This document outlines changes made by the IRS following an audit. If the IRS adjusts a taxpayer's return, including this report with the 511X can clarify the reasons for the amendment.

- Forms W-2 or 1099: These forms report income received during the tax year. If additional income was not included in the original return, new copies of these forms should be submitted to support the changes.

Using these forms and documents can help streamline the amendment process and reduce delays in processing your Oklahoma tax return. Always ensure that you include all necessary supporting documents to avoid any issues with your filing.

Guide to Using Oklahoma 511X

Completing the Oklahoma 511X form requires careful attention to detail. This amended tax return is used for correcting previous filings. Ensure that you have all necessary documents ready before starting the process.

- Obtain the Oklahoma 511X form for the appropriate tax year (2005 or earlier).

- Fill in your tax year at the top of the form.

- Enter your Social Security Number in the designated box.

- If applicable, check the box indicating if the taxpayer is deceased.

- Provide your first name, middle initial, and last name.

- If filing jointly, enter your spouse’s first name, middle initial, and last name.

- Input your current home address, including the apartment number or rural route.

- Enter your city, state, and zip code.

- Provide your phone number.

- Indicate if you filed an amended Federal return by checking "Yes" or "No."

- If you answered "Yes," attach a copy of IRS Form 1040X or 1045 and the Statement of Adjustment.

- Select your filing status on both the original and amended returns (Single, Married Filing Joint, or Married Filing Separate).

- List the number of exemptions claimed on both the original and amended returns.

- Check the box if you or your spouse are 65 or older.

- Indicate if you are not required to file a return due to insufficient gross income.

- Complete the income and deductions section, entering amounts as instructed.

- Calculate your Oklahoma adjusted gross income and adjustments as required.

- Determine your deductions and exemptions.

- Follow the instructions to calculate your tax liability.

- Fill in the payments section, detailing any Oklahoma income tax withheld or estimated tax paid.

- Calculate any refund or amount owed based on your entries.

- Provide explanations for any changes made in the appropriate sections.

- Sign and date the form. If filing jointly, both spouses must sign.

- Mail the completed form and all required documents to the Oklahoma Tax Commission at the specified address.