Fill in a Valid Oklahoma 512E Template

The Oklahoma 512E form is an important document for organizations seeking to report their tax-exempt status under Section 501(c) of the Internal Revenue Code. This form is specifically designed for organizations that are exempt from income tax but may have unrelated business income that is subject to taxation. It covers several key areas, including the identification of the organization, its federal employer identification number, and the type of return being filed—whether it’s an initial, final, or amended return. The form also requires organizations to report any unrelated business taxable income, along with deductions and credits applicable to Oklahoma tax law. Furthermore, it provides a section for organizations to make donations from their tax refunds to various causes, ranging from educational programs to support for veterans. Completing the 512E form accurately is crucial, as it ensures compliance with state tax regulations and helps maintain the organization’s tax-exempt status.

Document Properties

| Fact Name | Description |

|---|---|

| Form Purpose | The Oklahoma 512E form is used by organizations that are exempt from income tax under Section 501(c) of the Internal Revenue Code to report unrelated business taxable income. |

| Tax Year | This form is specifically for the tax year January 1 - December 31, 2020, or for another taxable year as applicable. |

| Filing Types | Organizations must indicate whether the return is an initial, final, or amended return by placing an 'X' in the appropriate box on the form. |

| Federal Employer Identification Number | Organizations must provide their Federal Employer Identification Number (FEIN) on the form to identify themselves for tax purposes. |

| Unrelated Business Income | Part 2 of the form requires organizations to report total unrelated trade or business income and deductions, which is crucial for calculating taxable income. |

| Tax Rate | The tax rate applied to unrelated business taxable income is 6%, as stipulated by Oklahoma law. |

| Oklahoma Statutes | The governing laws for the Oklahoma 512E form include 68 Oklahoma Statutes (OS) Sections 2368 and 2359, which outline filing requirements and tax obligations for exempt organizations. |

| Amended Returns | If filing an amended return, organizations must provide a copy of the amended Federal return and complete the Amended Return Schedule 512E-X. |

| Direct Deposit Requirement | All refunds must be issued via direct deposit, and organizations must provide banking information for this purpose on the form. |

| Donation Options | Organizations can choose to donate a portion of their refund to various Oklahoma funds, such as the Public School Classroom Support Fund or the Oklahoma General Revenue Fund. |

Common mistakes

-

Incorrectly marking the return type: Failing to check the appropriate box for whether the return is initial, final, or amended can lead to processing delays or errors.

-

Missing Federal Employer Identification Number (FEIN): Not providing the FEIN can result in rejection of the form, as this number is crucial for identification.

-

Inaccurate income reporting: Errors in reporting unrelated business taxable income can lead to incorrect tax calculations and potential penalties.

-

Omitting required attachments: Failing to include necessary documents, such as copies of federal returns or supporting schedules, may delay processing.

-

Incorrect calculation of tax: Miscalculating the tax due, especially when applying credits or deductions, can lead to overpayment or underpayment.

-

Neglecting to sign the form: An unsigned form is considered incomplete and will not be processed until it is signed.

-

Providing incorrect direct deposit information: Errors in the routing or account number can result in delays or failure of the direct deposit.

-

Not reviewing the instructions: Skipping the instructions can lead to misunderstandings about what is required, resulting in incomplete or incorrect submissions.

-

Failing to keep copies: Not retaining a copy of the submitted form and attachments can create issues if there are questions or disputes later.

-

Ignoring deadlines: Submitting the form after the deadline can result in penalties or interest on any taxes owed.

Popular PDF Documents

Ok Form 512 Instructions 2022 - Filing an amended return may result in a refund or additional tax liabilities.

For those interested in forming a limited liability company, understanding the vital role of an effective Operating Agreement template can streamline the process. Access the necessary resources for your company through our comprehensive Operating Agreement framework.

How Much Is Capital Gains Tax in Oklahoma - The 561NR assists in calculating the smaller amount of federal versus Oklahoma gains.

Misconceptions

Here are seven common misconceptions about the Oklahoma 512E form, along with clarifications to help you better understand this important tax document.

- Misconception 1: The 512E form is only for large organizations.

- Misconception 2: Filing the 512E form is optional for tax-exempt organizations.

- Misconception 3: Only organizations with profits need to worry about the 512E form.

- Misconception 4: The 512E form is the same as the federal Form 990.

- Misconception 5: You can file the 512E form anytime during the year.

- Misconception 6: You don’t need to attach any additional documents when filing the 512E form.

- Misconception 7: Once you file the 512E form, you don’t need to worry about it again until next year.

This form is required for any organization that qualifies for tax-exempt status under Section 501(c) of the Internal Revenue Code, regardless of size. Smaller organizations must also file if they have unrelated business income.

All tax-exempt organizations must file the 512E form each year, even if they have no unrelated business income. This ensures compliance with state tax laws.

Even if your organization operates at a loss, you still need to file the 512E form if you have unrelated business taxable income. This includes income from activities not directly related to your exempt purpose.

While both forms are related to tax-exempt organizations, they serve different purposes. The 512E form is specific to Oklahoma state tax obligations, while Form 990 is a federal requirement.

The 512E form must be filed by a specific deadline, usually 30 days after the due date established under federal law. Missing this deadline can lead to penalties.

If your organization has filed a federal return or has unrelated business income, you must attach relevant documents, such as Form 990 or 990-T, to your 512E form.

It’s essential to keep accurate records and stay informed about any changes in tax laws that may affect your organization. Regularly review your tax obligations to ensure compliance.

Preview - Oklahoma 512E Form

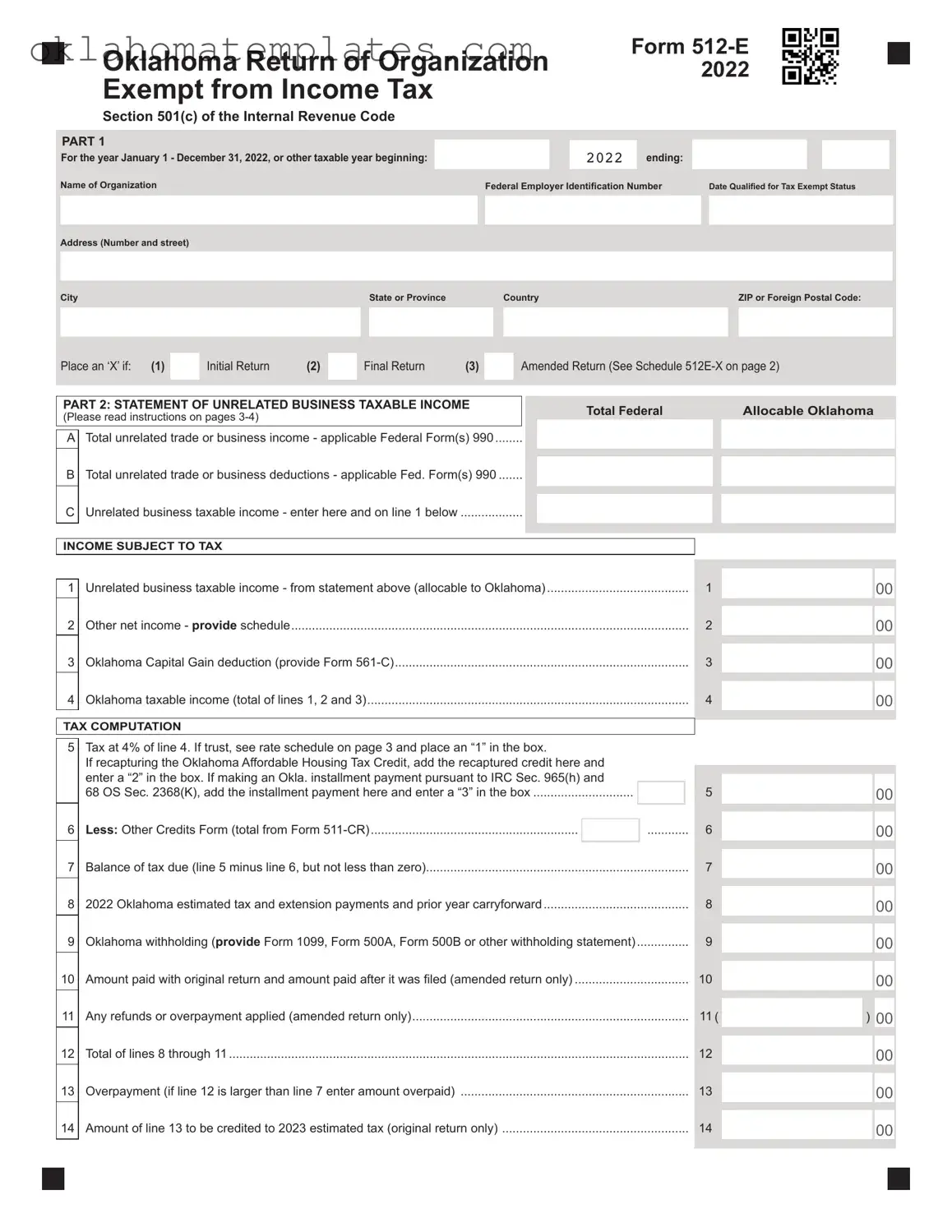

Oklahoma Return of Organization Exempt from Income Tax

Form

Section 501(c) of the Internal Revenue Code

PART 1

|

For the year January 1 - December 31, 2022, or other taxable year beginning: |

|

|

|

|

|

|

|

2022 ending: |

|

|

|

|

|

|

|

||||||||

Name of Organization |

|

|

|

|

|

|

|

|

Federal Employer Identification Number |

|

Date Qualified for Tax Exempt Status |

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address (Number and street) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

|

State or Province |

|

|

|

|

Country |

|

|

|

|

|

ZIP or Foreign Postal Code: |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Place an ‘X’ if: (1) |

|

Initial Return |

(2) |

|

|

Final Return |

(3) |

|

|

|

Amended Return (See Schedule |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

PART 2: STATEMENT OF UNRELATED BUSINESS TAXABLE INCOME |

|

|

|

|

|

Total Federal |

|

|

|

|

|

Allocable Oklahoma |

|

||||||||||

|

(Please read instructions on pages |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A Total unrelated trade or business income - applicable Federal Form(s) 990 |

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

B

Total unrelated trade or business deductions - applicable Fed. Form(s) 990 .......

C

Unrelated business taxable income - enter here and on line 1 below ..................

INCOME SUBJECT TO TAX

|

|

|

|

|

|

|

|

|

00 |

1 |

Unrelated business taxable income - from statement above (allocable to Oklahoma) |

1 |

|

|

|

|

|

|

|

2 |

Other net income - provide schedule |

2 |

|

00 |

|

|

|

|

|

3 |

Oklahoma Capital Gain deduction (provide Form |

3 |

|

00 |

|

|

|

|

|

4 |

Oklahoma taxable income (total of lines 1, 2 and 3) |

4 |

|

00 |

|

|

|

|

|

TAX COMPUTATION |

|

|

|

|

5

6

7

8

9

10

11

12

13

14

Tax at 4% of line 4. If trust, see rate schedule on page 3 and place an “1” in the box. |

|

|

|

|

|

|

|

|

|

|

If recapturing the Oklahoma Affordable Housing Tax Credit, add the recaptured credit here and |

|

|

|

|

|

|

|

|

|

|

enter a “2” in the box. If making an Okla. installment payment pursuant to IRC Sec. 965(h) and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

68 OS Sec. 2368(K), add the installment payment here and enter a “3” in the box |

|

|

5 |

|

|

|

00 |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Less: Other Credits Form (total from Form |

|

............ |

6 |

|

|

|

00 |

|

||

Balance of tax due (line 5 minus line 6, but not less than zero) |

|

7 |

|

|

|

|

|

|

||

|

|

|

|

00 |

|

|||||

2022 Oklahoma estimated tax and extension payments and prior year carryforward |

|

8 |

|

|

|

|

|

|||

|

|

|

00 |

|

||||||

Oklahoma withholding (provide Form 1099, Form 500A, Form 500B or other withholding statement) |

|

|

9 |

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||

Amount paid with original return and amount paid after it was filed (amended return only) |

|

10 |

|

|

|

|

|

|

||

|

|

|

|

00 |

|

|||||

Any refunds or overpayment applied (amended return only) |

|

11 |

( |

|

|

|

|

|||

|

|

) |

00 |

|

||||||

Total of lines 8 through 11 |

|

12 |

|

|

|

|

|

|||

|

|

|

00 |

|

||||||

Overpayment (if line 12 is larger than line 7 enter amount overpaid) |

|

13 |

|

|

|

|

|

|

||

|

|

|

|

00 |

|

|||||

Amount of line 13 to be credited to 2023 estimated tax (original return only) |

|

14 |

|

|

|

|

|

|

||

|

|

|

00 |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

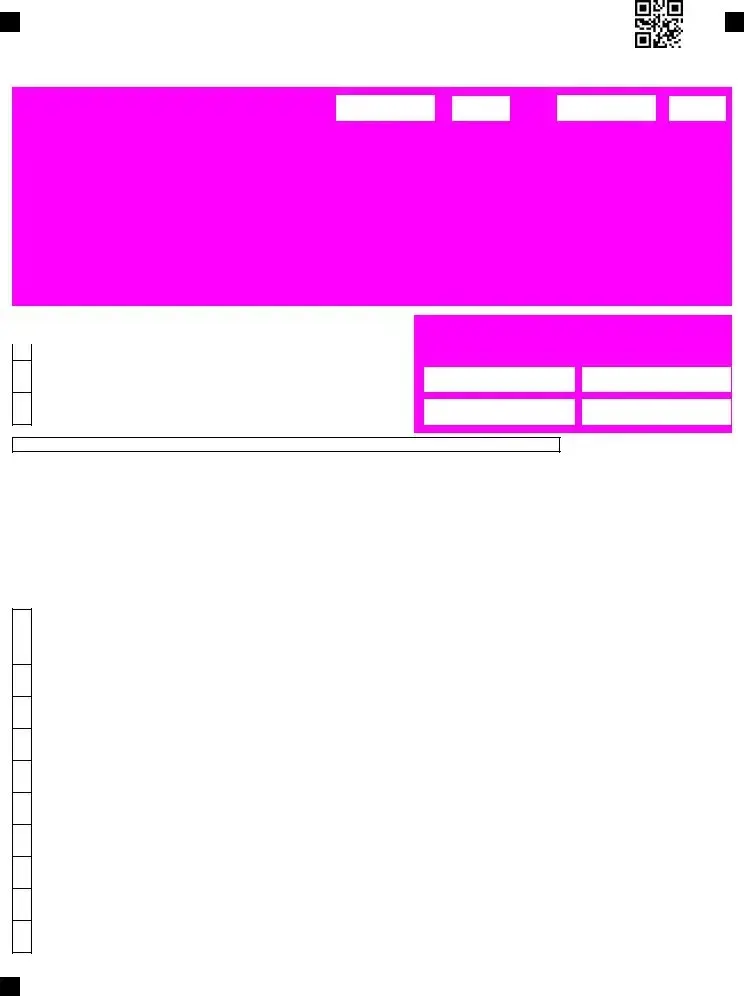

2022 Form

Oklahoma Return of Organization Exempt from Income Tax

Name of Organization::

Federal Employer Identification Number:

Amount from line 14 on page 1 |

|

|

|

|

|

00 |

|

|

|

|

|

Line 15 provides you the opportunity to make a financial gift from your refund to a variety of Oklahoma organizations. Place the line number of the organization from page 4 of this form in the box below and enter the amount you are donating. If giving to more than one organization, put a “99” in the box and attach a schedule showing how you would like your donation split.

15

16

17

Donations from your refund |

|

$2 |

|

$5 |

|

$ ________________ |

|

|

15 |

|

|

|

|

|

|

|

|

|

|

Add lines 14 and 15 and enter amount |

|

|

|

|

|

|

16 |

||

Amount to be refunded to you (line 13 minus line 16) |

|

|

|

|

Refund |

17 |

|||

00

00

00

00

00

00

Direct Deposit Note:

All refunds must be by direct deposit. See Direct Deposit Information on page 5 for details.

Is this refund going to or through an account that is located outside of the United States?  Yes

Yes  No

No

Deposit my refund in my: |

|

Checking Account |

|

Savings Account |

|

|

|

|

|

Routing Number:

Account Number:

|

|

|

|

|

|

|

|

|

........................................................................... |

Tax Due |

|

|

00 |

||

18 |

Tax Due (if line 7 is larger than line 12 enter tax due) |

18 |

|

||||

|

|

|

|

|

|

|

|

19 |

Donation: Public School Classroom Support Fund (For information regarding this fund, see page 4, #5) |

19 |

|

00 |

|||

|

|

|

|

|

|

|

|

20 |

For delinquent payment, add penalty of 5% plus interest at 1.25% per month |

|

|

20 |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

21 |

Underpayment of estimated tax interest |

Annualized |

|

|

21 |

|

|

22 |

Total tax, penalty and interest due - Add lines |

Balance Due |

22 |

|

00 |

||

|

|

|

|

|

|

|

|

Under penalty of perjury, I declare the information contained in this document, attachments and schedules are true and correct to the best of my knowledge and belief.

Signature of Office or Trustee |

Date |

|

|

Printed Name |

|

|

|

Title |

Phone Number |

|

|

Check this box if the Oklahoma Tax Commission may discuss this return with your tax preparer.

Signature of Preparer |

Date |

|

|

Printed Name of Preparer |

|

|

|

Phone Number |

Preparer’s PTIN |

|

|

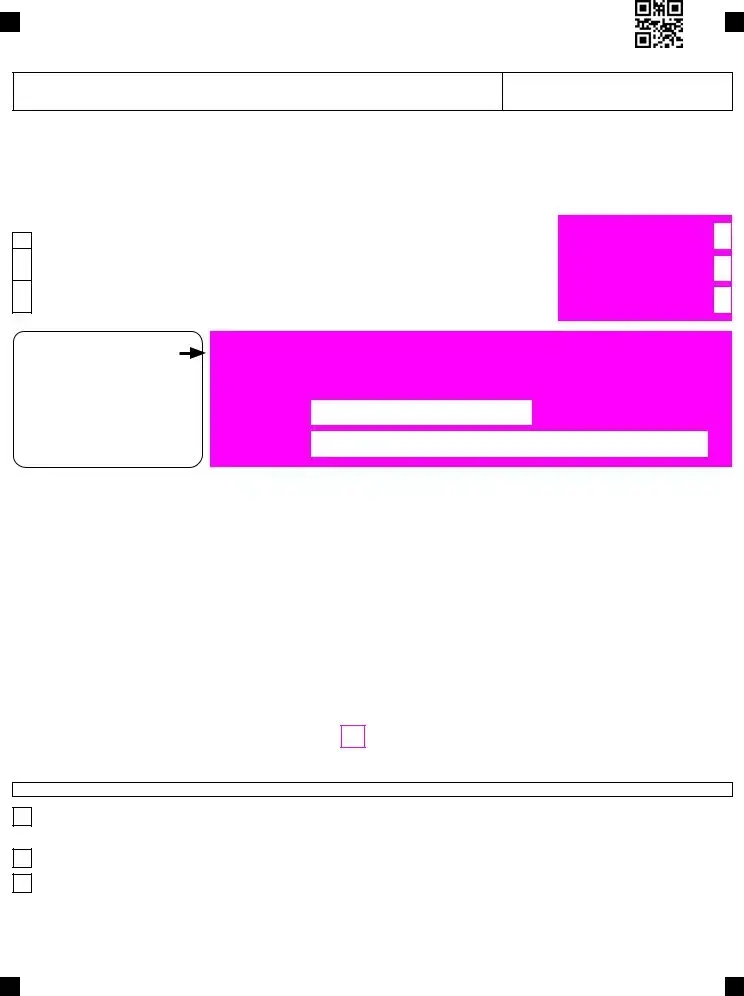

SCHEDULE

A

B

C

Did you file an amended Federal income tax return? |

|

Yes |

|

No |

Provide a copy of the amended Federal return and a copy of “Statement of Adjustment”, IRS refund check or deposit slip.

If this return is being filed due to a Federal audit, provide a complete copy of the RAR.

Explanation or reason for amended return (Provide all necessary schedules):

________________________________________________________________________________________________________________

________________________________________________________________________________________________________________

The Oklahoma Tax Commission is not required to give actual notice to taxpayers of changes in any state tax law.

2022 Form

Instructions for Filing an Amended Return

When filing an amended return, place an “X” in the Amended return

11. Complete the Amended Return Schedule, Schedule

Provide the amended Federal return and proof of disposition by the Internal Revenue Service (IRS) when applicable.

An overpayment on an amended return may not be credited to estimated tax, but will be refunded. The amount applied to estimated tax on the original return cannot be adjusted.

General Instructions

Every organization shall make a return for each year. 68 Oklahoma Statutes (OS) Section 2368.

Part 1 and the signature section must be completed by all organizations. If you were required to file an annual information return with the IRS, enclose a copy of the information return including any supporting schedules (e.g. Form 990,

Part 2 is to be completed by organizations who have unrelated trade or business income. If you were required to file an income tax return with the IRS, enclose a copy of the tax return including any supporting schedules (e.g. Form

Corporate returns shall be due no later than 30 days after the due date established under the Internal Revenue Code (IRC).

Exempt Organizations are subject to tax on unrelated business income. 68 OS Sec. 2359.

Investment income of exempt organizations subject to federal excise tax is not subject to Oklahoma income tax; however, any income subject to income tax under the IRC is subject to Oklahoma income tax.

Complete the Oklahoma Statement of Unrelated Business Income and attach a schedule of any other taxable income.

Total unrelated trade or business deductions includes the “specific deduction” allowed on the Federal return.

If you do not have a Federal Employer Identification Number, you may obtain one by visiting the IRS website at irs.gov.

If you are a member, either directly or indirectly, of an electing

PTE, federal identification number, the year of the election, federal taxable income (loss) and Oklahoma taxable income (loss) that is covered by the election pursuant to this Act. Also provide a copy of the OTC acknowledgement letter received by the PTE. 68 OS Sec.

Line 5 - TAX

The income tax rate is 4%.

Trust: If the exempt organization is a trust, the following rates apply. Enter a “1” in the box on Form

If taxable income is: At least |

- |

But less than |

|

|

|

|

|

|

||

- |

1,000 |

|

Pay |

0.00 |

+ |

0.25% |

over |

.................... 0 |

||

|

|

|

|

|

|

|

|

|

|

|

1,001 |

- |

2,500 |

|

Pay |

2.50 |

+ |

0.75% |

over |

............. 1,000 |

|

|

|

|

|

|

|

|

|

|

|

|

2,501 |

- |

3,750 |

|

Pay |

13.75 |

+ |

1.75% |

over |

............. 2,500 |

|

|

|

|

|

|

|

|

|

|

|

|

3,751 |

- |

4,900 |

|

Pay |

35.63 |

+ |

2.75% |

over |

............. 3,750 |

|

|

|

|

|

|

|

|

|

|

|

|

4,901 |

- |

7,200 |

|

Pay |

67.25 |

+ |

3.75% |

over |

............. 4,900 |

|

|

|

|

|

|

|

|

|

|

|

|

7,201 |

|

over |

Pay |

153.50 |

+ |

4.75% |

over |

............. 7,200 |

||

Recapture of the Oklahoma Affordable Housing Tax Credit:

If under IRC Section 42 a portion of any federal

to such project shall also be required to recapture a portion of such credits. The amount of Oklahoma Affordable Housing Tax Credits subject to recapture is proportionally equal to the amount of federal

Making an Oklahoma installment payment pursuant to IRC Section 965(h):

If a taxpayer elected to make installment payments of tax due pursuant to the provisions of subsection (h) of Section 965 of the IRC, such election may also apply to the payment of Oklahoma income tax, attributable to the income upon which such installment payments are based. Add the installment payment to the Oklahoma income tax and enter a “3” in the box on Form

Mail to: Oklahoma Tax Commission • PO Box 26800 • Oklahoma City, OK

2022 Form

Donations from Refund

1 - Support of Programs for Volunteers to Act as Court Appointed Special Advocates for Abused or Neglected Children

You may donate from your tax refund to support programs for volunteers to act as Court Appointed Special Advocates for abused

or neglected children. Donations will be placed in the Income Tax Checkoff Revolving Fund for Court Appointed Special Advocates.

Monies will be expended by the Office of the Attorney General for the purpose of providing grants to the Oklahoma CASA Association. If you are not receiving a refund, you may still donate. Mail your contribution to: Oklahoma CASA Association, Inc., PO Box 54946, Oklahoma City, OK 73154.

2 - Y.M.C.A. Youth and Government Program

You may donate from your tax refund to support the Oklahoma chapter of the Y.M.C.A. Youth and Government program. Monies donated will be expended by the State Department of Education for the purpose of providing grants to the Program so young people

may be educated regarding government and the legislative process. If you are not receiving a refund, you may still donate. Mail your contribution to: Oklahoma State Department of Education, Y.M.C.A. Youth and Government Program, Office of the Comptroller, 2500 North Lincoln Boulevard, Room 415, Oklahoma City, OK

3 - Support the Wildlife Diversity Fund

You may donate from your tax refund to support the conservation of rare or declining fish and wildlife along with common species not hunted or fished. Donations to the Oklahoma Department of Wildlife Conservation’s Wildlife Diversity program supports field surveys

of animals considered to be of greatest conservation need, as well as educational wildlife programs for all Oklahomans. Tax deductible donations to the Wildlife Diversity Fund also can be made at wildlifedepartment.com or by mail: Oklahoma Department of Wildlife Conservation, Re: Wildlife Diverstiy Fund, PO Box 53465, Oklahoma City, Oklahoma 73152.

4 - Support of Programs for Regional Food Banks in Oklahoma

You may donate from your tax refund to support the Regional Food Bank of Oklahoma and the Community Food Bank of Eastern

Oklahoma (Oklahoma Food Banks). The Oklahoma Food Banks are the largest

food to the more than 500,000 Oklahomans at risk of hunger on a daily basis. If you are not receiving a refund, you may still donate. Mail your contribution to: Oklahoma Department of Human Services, Revenue Processing Unit, Re: Programs for OK Food Banks, PO Box 248893, Oklahoma City, OK 73124.

5 - Public School Classroom Support Fund

You may donate from your tax refund to support the Public School Classroom Support Revolving Fund, which will be used by the State Board of Education to provide one or more grants annually to public school classroom teachers. Grants will be used by the classroom

teacher for supplies, materials, or equipment for the class or classes taught by the teacher. Grant applications will be considered on a statewide competitive basis. You may also mail a donation to: Oklahoma State Board of Education, Public School Classroom Support Fund, Office of the Comptroller, 2500 North Lincoln Boulevard, Room 415, Oklahoma City, OK

6 - Oklahoma Pet Overpopulation Fund

You may donate from your tax refund to support the Oklahoma Pet Overpopulation Fund. Monies placed in this fund will be expended

for the purpose of developing educational programs on pet overpopulation and for implementing spay/neuter efforts in this state. If you are not receiving a refund, you may still donate. Mail your contribution to: Oklahoma Department of Agriculture, Food and Forestry,

Animal Industry Division, 2800 North Lincoln Boulevard, Oklahoma City, OK 73105.

7 - Support the Oklahoma AIDS Care Fund

You may donate from your tax refund to support the Oklahoma AIDS Care Fund. Monies will be expended by the Department of Human

Services for the purpose of providing grants to the Fund for purposes of emergency assistance, advocacy, education, prevention and collaboration with other entities. If you are not receiving a refund, you may still donate. Mail your contribution to: Oklahoma Department of Human Services, Revenue Processing Unit, Re: OK Aids Care Fund, PO Box 248893, Oklahoma City, OK 73124.

8- Oklahoma Silver Haired Legislature and Alumni Association Programs

You may donate from your tax refund to support the Oklahoma Silver Haired Legislature and their Alumni Association activities. The Oklahoma Silver Haired Legislature was created in 1981 as a forum to educate senior citizens in the legislative process and to highlight the needs of older persons to the Oklahoma State Legislature. Monies generated from donations will be used to fund expenses of

the Silver Haired Legislators, training sessions, interim studies and advocacy activities. If you are not receiving a refund, you may still donate. Mail your contribution to: Oklahoma Silver Haired Legislature and Alumni, PO Box 25352, Oklahoma City, OK 73125.

2022 Form

Direct Deposit Information

Complete the direct deposit section on the tax return to have the refund directly deposited into your account at a bank or financial institution. Refunds, with limited exceptions, must be made by direct deposit.

1Place an ‘X’ in the appropriate box as to whether the refund will be going into a checking or savings account. Please keep in mind you will not receive notification of the deposit.

2Fill out the routing number. The routing number must be nine digits. Using the sample check shown below, the routing number is 120120012. If the first two digits are not 01 through 12 or 21 through 32, the direct deposit will fail to process.

3Enter your account number. The account number can be up to 17 characters (both numbers and letters). Include hyphens but omit spaces and special symbols. Enter the number from left to right. On the sample check shown below, the account number is 2020268620.

Please Note: The OTC is not responsible if a financial institution refused a direct deposit. If a direct deposit is refused, a check

will be issued to the address shown on the tax return.

WARNING! Due to electronic banking rules, the OTC will NOT allow direct deposits to or through foreign financial institutions. If you use a foreign financial institution, you will be issued a paper check.

ABC Corporation |

1234 |

|

||

123 Main Street |

|

|||

Anyplace, OK 00000 |

|

Account |

||

|

|

|

||

PAY TO THE |

SAMPLE |

$ |

Number |

|

ORDER OF |

|

|||

Routing |

|

DOLLARS |

|

|

Number |

|

|

||

|

|

|

||

ANYPLACE BANK |

|

|

||

Anyplace, OK 00000 |

SAMPLE |

Note: The routing |

||

|

|

|||

For |

|

and account numbers |

||

|

may appear in |

|||

|

|

|

||

:120120012 : 2020268620 |

1234 |

different places on |

||

your check. |

||||

|

|

|

||

FAQ

What is the purpose of the Oklahoma 512E form?

The Oklahoma 512E form is designed for organizations that are exempt from federal income tax under Section 501(c) of the Internal Revenue Code. This form allows these organizations to report any unrelated business taxable income (UBTI) they may have earned during the tax year. It ensures compliance with Oklahoma tax laws and helps determine any tax liabilities associated with that income.

Who needs to file the Oklahoma 512E form?

Any organization that has received tax-exempt status under Section 501(c) and has generated unrelated business income must file the Oklahoma 512E form. This includes charities, educational institutions, and other nonprofit entities. Even if the organization is generally exempt from income tax, it must report UBTI and may owe taxes on that income.

How is unrelated business taxable income calculated on the form?

To calculate unrelated business taxable income, the organization must first determine its total unrelated trade or business income. This is done by referencing the applicable Federal Form(s) 990. Next, the organization must subtract total unrelated trade or business deductions, also taken from the same Federal Form(s). The resulting figure is the unrelated business taxable income, which is reported on the Oklahoma 512E form.

What are the key deadlines for filing the Oklahoma 512E form?

The Oklahoma 512E form must be filed no later than 30 days after the due date established under the Internal Revenue Code for the organization’s annual information return. It’s crucial for organizations to adhere to this deadline to avoid penalties and interest on any taxes owed.

Can organizations make donations from their tax refunds when filing the Oklahoma 512E?

Yes, organizations have the option to donate a portion of their tax refund to various Oklahoma programs when filing the Oklahoma 512E form. There are several designated funds, such as the Public School Classroom Support Fund and the Oklahoma Emergency Responders Assistance Program. Organizations can specify the amount and the fund to which they wish to contribute directly on the form.

Documents used along the form

When navigating the world of tax-exempt organizations in Oklahoma, the Oklahoma 512E form is just one of several important documents you may encounter. Each of these forms serves a specific purpose and can be essential for ensuring compliance with state and federal regulations. Here’s a brief overview of other forms and documents commonly used alongside the Oklahoma 512E.

- Form 990: This is the annual information return filed by tax-exempt organizations. It provides detailed information about the organization's finances, activities, and governance. Organizations with gross receipts over a certain threshold must file this form.

- Form 990-EZ: A shorter version of Form 990, this form is available for smaller tax-exempt organizations with gross receipts below a specific limit. It simplifies reporting while still capturing essential financial data.

- Form 990-PF: Private foundations use this form to report their financial activities, including income, expenses, and distributions. It ensures transparency and compliance with IRS regulations.

- Schedule A: Attached to Form 990, this schedule is used to provide additional information about the organization’s public charity status and to demonstrate compliance with public support tests.

- Form 561-C: This form is used to claim the Oklahoma Capital Gain deduction. Organizations must provide details about capital gains and related transactions to benefit from this deduction.

- Form 511CR: This is the Oklahoma Credit form, which allows organizations to claim various tax credits. It’s essential for maximizing potential savings on state taxes.

- Form 1099: This form is used to report various types of income other than wages, salaries, and tips. Organizations may need to issue Form 1099 to report payments made to independent contractors or other service providers.

- Texas Quitclaim Deed: A legal document used to transfer any interest in real property without guaranteeing the title's validity. For more information, you can refer to UsaLawDocs.com.

- Schedule 512E-X: This is the Amended Return Schedule that organizations use if they need to make corrections to a previously filed Form 512E. It helps ensure that all information is accurate and up-to-date.

Understanding these forms and their purposes can greatly assist organizations in maintaining compliance and managing their tax obligations effectively. Each document plays a role in the larger framework of tax reporting and can help ensure that your organization remains in good standing with both state and federal authorities.

Guide to Using Oklahoma 512E

Filling out the Oklahoma 512E form is an essential step for organizations seeking to maintain their tax-exempt status while reporting any unrelated business income. This process requires careful attention to detail to ensure compliance with state regulations. Follow the steps below to complete the form accurately.

- Begin by indicating the tax year at the top of the form. Mark an ‘X’ in the appropriate boxes for initial, final, or amended return.

- Provide the name of your organization and its Federal Employer Identification Number (FEIN).

- Fill in the address of the organization, including the street number and name, city, state, and ZIP code.

- Enter the date your organization qualified for tax-exempt status.

- In Part 2, report the total unrelated trade or business income and deductions as per the applicable Federal Form(s) 990.

- Calculate the unrelated business taxable income and enter it in the designated space.

- Complete the income subject to tax section by adding any other net income and Oklahoma capital gain deductions.

- Calculate the total Oklahoma taxable income by summing the amounts from the previous step.

- Determine the tax due by calculating 6% of the Oklahoma taxable income. If applicable, mark any relevant boxes for trusts or recapturing credits.

- Subtract any other credits from the tax due to find the balance of tax owed.

- List any estimated tax payments, withholding amounts, and any payments made with the original return or after filing.

- Calculate the total of lines for estimated payments and refunds to determine any overpayment or amount to be refunded.

- If you wish to donate from your refund, enter the organization number and the donation amount in the appropriate section.

- Complete the direct deposit section by selecting whether the refund will go into a checking or savings account and providing the necessary routing and account numbers.

- Sign and date the form, ensuring that the information provided is accurate to the best of your knowledge.

After filling out the form, review it thoroughly to ensure all information is correct. Once completed, mail the form to the Oklahoma Tax Commission at the specified address. Keeping a copy for your records is advisable. This will help in case of any future inquiries or audits.