Fill in a Valid Oklahoma 538 S Template

The Oklahoma 538 S form serves as a crucial tool for residents seeking relief from sales tax burdens. Specifically designed for individuals and households with a gross income of $12,000 or less, this form allows eligible taxpayers to claim a refund or credit for sales tax paid during the year. To successfully complete the form, applicants must provide personal information, including names, addresses, and Social Security numbers, as well as details about their dependents. The eligibility criteria are strict; for instance, individuals who received Aid to Families with Dependent Children (A.F.D.C.) during the year are disqualified from receiving a refund. Additionally, applicants must demonstrate continuous residency in Oklahoma throughout the year and accurately report all household income, which encompasses various sources such as wages, pensions, and public assistance. The form also outlines the necessary calculations for determining the total exemptions claimed, which directly influence the refund amount. It is essential to follow the instructions carefully, as incomplete submissions may result in delays. Overall, the Oklahoma 538 S form plays a vital role in supporting low-income residents by providing a pathway to financial relief through tax credits and refunds.

Document Properties

| Fact Name | Details |

|---|---|

| Form Title | Oklahoma Claim for Credit or Refund of Sales Tax 538-S |

| Eligibility Requirements | Applicants must be Oklahoma residents for the entire year and have a gross household income not exceeding $12,000. |

| Exemption Amount | The credit is $40 for each qualified personal exemption and dependent claimed. |

| Ineligibility Notice | Individuals who received Aid for Dependent Children (A.F.D.C.) in 1996 are not eligible for the refund. |

| Submission Deadline | The form must be submitted by June 30 of the year following the tax year if not filing an income tax return. |

| Governing Law | The form is governed by Oklahoma state tax laws, specifically those relating to sales tax refunds. |

Common mistakes

-

Incomplete Information: Many individuals fail to provide all required information on the form. Missing details such as Social Security numbers, names, or income sources can lead to delays or denials of the refund.

-

Incorrect Income Reporting: Some people misreport their total household income. It is crucial to include all types of income, both taxable and nontaxable, to ensure accurate calculations.

-

Failure to Check Eligibility: Applicants often overlook eligibility requirements. For instance, those who received Aid to Families with Dependent Children (A.F.D.C.) during the year are not eligible for a refund.

-

Missing Signatures: A common mistake is neglecting to sign and date the form. Both the taxpayer and spouse must provide their signatures for the application to be valid.

-

Ignoring Deadlines: Many individuals submit their forms late. It is essential to remember that the form must be received by the Oklahoma Tax Commission by June 30 following the tax year, or it will not be processed.

Popular PDF Documents

File Oklahoma Taxes Online - The longer 511 form allows for more complex filings, including multiple deductions.

Understanding the importance of a reliable Power of Attorney document is vital for anyone looking to ensure their financial and medical wishes are met. For those interested in learning more, you can find a helpful resource that discusses the experience of creating a "legal Power of Attorney form" at this link.

Oklahoma Nonresident Income Tax - Height, weight, pulse, and blood pressure measurements form part of the initial health assessment.

Misconceptions

Understanding the Oklahoma 538 S form is crucial for those seeking a sales tax refund. However, several misconceptions can lead to confusion and mistakes. Here are ten common misconceptions clarified.

- Only low-income individuals can apply. Many believe that only those with very low incomes qualify. While the income threshold is set at $12,000, other factors also determine eligibility.

- All residents qualify for the refund. Not all residents are eligible. For instance, individuals who have received Aid to Families with Dependent Children (A.F.D.C.) during the year are disqualified.

- The form can be submitted anytime. There is a strict deadline. The form must be submitted by June 30 of the year following the tax year.

- Dependents do not need to be listed. All dependents must be listed with accurate information, including Social Security numbers and income, if applicable.

- Blindness or age exemptions apply. There are no exemptions for blindness or for individuals aged 65 and over in this context.

- Filing an income tax return is not necessary. If you are required to file an income tax return, you must include the credit from the 538 S form on your tax return.

- Only Oklahoma residents qualify. Individuals living in Oklahoma under a visa do not qualify for the sales tax credit or refund.

- The refund is automatic. The refund is not automatic. Applicants must complete the form accurately and submit it on time.

- Income types are irrelevant. All income types, taxable or not, must be reported, including pensions, social security, and unemployment benefits.

- Death of a taxpayer disqualifies the claim. If a taxpayer or spouse dies during the tax year, the refund may still be issued to their estate if the form is filed correctly.

Addressing these misconceptions can help individuals better navigate the application process and ensure they receive the credits and refunds they are entitled to.

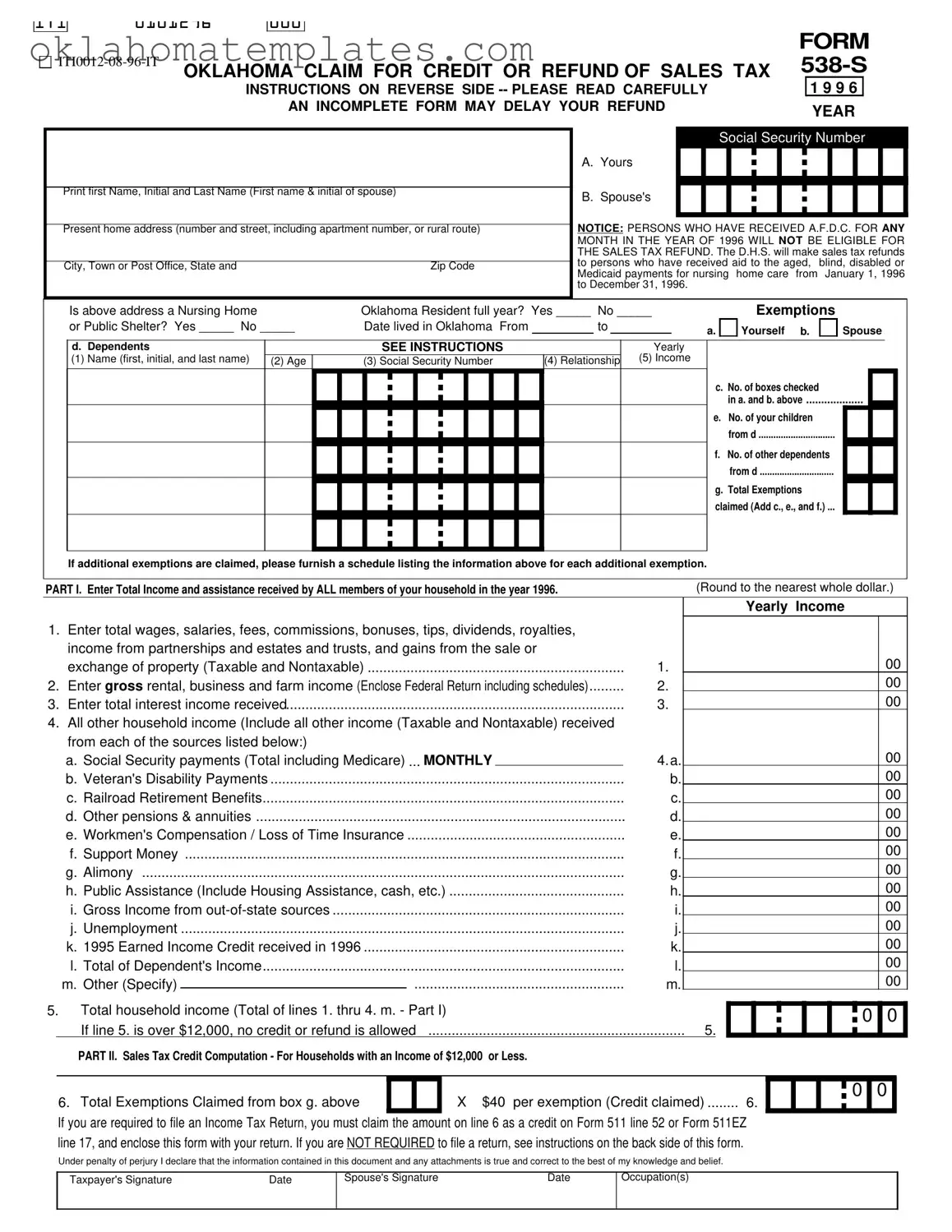

Preview - Oklahoma 538 S Form

ITI |

0101296 |

000 |

|

|

|

|

|

|

FORM |

OKLAHOMA CLAIM FOR CREDIT OR REFUND OF SALES TAX |

||||

|

|

1 9 9 6 |

||

|

|

|

INSTRUCTIONS ON REVERSE SIDE |

|

|

|

|

AN INCOMPLETE FORM MAY DELAY YOUR REFUND |

YEAR |

|

|

|

|

|

Print first Name, Initial and Last Name (First name & initial of spouse)

Present home address (number and street, including apartment number, or rural route)

City, Town or Post Office, State and |

Zip Code |

Social Security Number

A. Yours

B. Spouse's

NOTICE: PERSONS WHO HAVE RECEIVED A.F.D.C. FOR ANY

MONTH IN THE YEAR OF 1996 WILL NOT BE ELIGIBLE FOR THE SALES TAX REFUND. The D.H.S. will make sales tax refunds to persons who have received aid to the aged, blind, disabled or Medicaid payments for nursing home care from January 1, 1996 to December 31, 1996.

Is above address a Nursing Home |

Oklahoma Resident full year? Yes _____ No _____ |

|

or Public Shelter? Yes _____ No _____ |

Date lived in Oklahoma From |

to |

d. Dependents |

SEE INSTRUCTIONS |

Yearly |

(1) Name (first, initial, and last name) (2) Age |

(3) Social Security Number |

(4) Relationship (5) Income |

Exemptions

a.

Yourself b.

Yourself b.

Spouse

Spouse

c. No. of boxes checked

in a. and b. above ...................

e.No. of your children from d ...............................

f.No. of other dependents from d ..............................

g.Total Exemptions claimed (Add c., e., and f.) ...

If additional exemptions are claimed, please furnish a schedule listing the information above for each additional exemption.

PART I. Enter Total Income and assistance received by ALL members of your household in the year 1996.

1.Enter total wages, salaries, fees, commissions, bonuses, tips, dividends, royalties, income from partnerships and estates and trusts, and gains from the sale or

(Round to the nearest whole dollar.)

Yearly Income

|

exchange of property (Taxable and Nontaxable) |

1. |

2. |

Enter gross rental, business and farm income (Enclose Federal Return including schedules) |

2. |

3. |

Enter total interest income received |

3. |

4.All other household income (Include all other income (Taxable and Nontaxable) received from each of the sources listed below:)

a. |

Social Security payments (Total including Medicare) ... MONTHLY |

4. a. |

b. |

Veteran's Disability Payments |

b. |

c. |

Railroad Retirement Benefits |

c. |

d. |

Other pensions & annuities |

d. |

e. |

Workmen's Compensation / Loss of Time Insurance |

e. |

f. |

Support Money |

f. |

g. |

Alimony |

g. |

h. |

Public Assistance (Include Housing Assistance, cash, etc.) |

h. |

i. |

Gross Income from |

i. |

j. |

Unemployment |

j. |

k. |

1995 Earned Income Credit received in 1996 |

k. |

l. |

Total of Dependent's Income |

l. |

m. |

Other (Specify) |

m. |

5.Total household income (Total of lines 1. thru 4. m. - Part I)

If line 5. is over $12,000, no credit or refund is allowed ..................................................................

PART II. Sales Tax Credit Computation - For Households with an Income of $12,000 or Less.

5.

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

0

0  0

0

6. Total Exemptions Claimed from box g. above |

|

0 |

0 |

||

X $40 per exemption (Credit claimed) ........ 6. |

|

||||

If you are required to file an Income Tax Return, you must claim the amount on line 6 as a credit on Form 511 line 52 or Form 511EZ |

|

||||

line 17, and enclose this form with your return. If you are NOT REQUIRED to file a return, see instructions on the back side of this form. |

|

||||

Under penalty of perjury I declare that the information contained in this document and any attachments is true and correct to the best of my knowledge and belief. |

|

||||

Taxpayer's Signature |

Date |

Spouse's Signature |

Date |

Occupation(s) |

|

NOTICE

THE DEPARTMENT OF HUMAN SERVICES (D.H.S.) WILL MAKE SALES TAX REFUNDS TO PERSONS WHO HAVE CONTINUOUSLY RECEIVED AID TO THE AGED, BLIND, DISABLED OR MEDICAID PAYMENTS FOR NURSING HOME CARE FROM JANUARY 1, 1996 TO DECEMBER 31, 1996.

PERSONS WHO HAVE RECEIVED AID FOR DEPENDENT CHILDREN (A.F.D.C.) FOR ANY MONTH IN THE YEAR OF 1996 WILL NOT BE ELIGIBLE FOR THE SALES TAX CREDIT OR REFUND.

INSTRUCTIONS

Beginning in 1990, anyone who is an Oklahoma resident and lives in Oklahoma for the entire year and whose gross household income does not exceed Twelve Thousand Dollars ($12,000) may file for sales tax relief.

For 1996 the amount shall be Forty Dollars ($40) multiplied by the number of qualified personal exemptions and qualified dependents to which you would be entitled for Oklahoma Income Tax.

EXCEPTIONS:

There is no exemption for blindness.

There is no exemption for age

A person convicted of a felony shall not be permitted to file a claim for sales tax relief for any period of time during which the person is an inmate in the custody of the Department of Corrections.

Individuals living in Oklahoma under a Visa will not qualify for the sales tax credit or refund.

If a taxpayer or spouse died during the tax year, they will not qualify for the sales tax credit or refund. If a taxpayer or spouse died after 12/31/96, but before this tax form was filed, the sales tax credit or refund for the deceased will be issued to their estate. Please indicate date of death.

If using an

To qualify as a dependent for the sales tax credit or refund, you must qualify and be claimed as a dependent for Federal Income Tax purposes. THE NAME, SOCIAL SECURITY NUMBER, AGE, RELATIONSHIP AND YEARLY INCOME (if any) MUST BE ENTERED FOR ALL DEPENDENTS. All other sales tax credit or refund requirements must also be met to qualify (Example: Resident of and lives in Oklahoma for entire year).

DEPENDENT CHILD: Enter Age and Social Security Number for all dependents. If nineteen (19) years of age, or over, enter age and “D” if disabled, or “S” if a Student. CHECK ALL SOCIAL SECURITY NUMBERS FOR ACCURACY.

OTHER DEPENDENT: A dependent on the Federal return other than your child.

For this form the “Gross Household Income” means the amount of income of every type, regardless of the source (except for gifts) received by ALL persons living in the same household, whether the income was taxable or not for income tax purposes. This includes pensions, annuities, social security, unemployment payments, veteran’s disability compensation, school grants or scholarships, public assistance payments, alimony, support money, workmen’s compensation,

If you are required to file an Oklahoma State Income Tax Return, you must claim the amount of line 6., Part II, as a credit on your tax return

If you are NOT required to file an Oklahoma State Income Tax Return, this form must be received by the Oklahoma Tax Commission on or before the 30th day of June following the close of the taxable year. If you have withholding or made a payment on estimate and are filing for a refund on Form 511RF, you must enclose this form with the 511RF; otherwise, complete, sign, and date this form and mail your completed form to: Oklahoma Tax Commission, Income Tax, 2501 Lincoln Blvd., Oklahoma City, Ok

All information must be furnished or the processing of your claim or refund will be delayed.

FAQ

What is the purpose of the Oklahoma 538 S form?

The Oklahoma 538 S form is used to claim a credit or refund for sales tax for eligible residents. Specifically, it is intended for individuals whose gross household income does not exceed $12,000 for the year 1996. The form allows qualifying residents to receive a refund based on the number of personal exemptions and dependents they claim, with a maximum credit of $40 per exemption. This program aims to provide financial relief to low-income households in Oklahoma.

Who is eligible to file the Oklahoma 538 S form?

Eligibility for the Oklahoma 538 S form is contingent upon several factors. To qualify, you must be an Oklahoma resident who lived in the state for the entire year of 1996. Your gross household income must not exceed $12,000. Additionally, you cannot have received Aid for Dependent Children (A.F.D.C.) during any month of that year. Exceptions apply to individuals receiving aid for the aged, blind, disabled, or Medicaid payments for nursing home care. It's also important to note that individuals convicted of a felony or those living in Oklahoma under a visa do not qualify.

What information is required to complete the form?

To complete the Oklahoma 538 S form, you will need to provide various personal details, including your name, address, and Social Security number. You must also list the names, ages, Social Security numbers, and relationships of all dependents. Additionally, you will need to report your total household income, which includes wages, benefits, and any other sources of income for all members of your household. Accurate and complete information is crucial, as any omissions may delay your refund.

What happens if I miss the filing deadline for the Oklahoma 538 S form?

Filing deadlines are strict for the Oklahoma 538 S form. If you are required to file an Oklahoma State Income Tax Return, you must submit the form along with your return by April 15th of the following year. If you are not required to file a return, your completed form must be received by the Oklahoma Tax Commission by June 30th following the close of the tax year. Missing these deadlines could result in the loss of your opportunity to claim the sales tax credit or refund.

How do I submit the Oklahoma 538 S form?

You can submit the Oklahoma 538 S form by mailing it to the Oklahoma Tax Commission. If you are filing it with your Oklahoma Individual Income Tax Return, include it with your return using the address provided on the tax return. If you are not required to file a return, send the completed form directly to the Oklahoma Tax Commission at 2501 Lincoln Blvd., Oklahoma City, OK 73194-0009. Ensure that the form is signed and dated, as incomplete submissions may cause delays in processing your claim.

Documents used along the form

When filing the Oklahoma 538 S form, several other documents may be necessary to support your claim for a sales tax credit or refund. Each document plays a vital role in ensuring that your application is complete and accurate. Below is a list of commonly used forms and documents that may accompany the Oklahoma 538 S form.

- Oklahoma Individual Income Tax Return (Form 511 or 511EZ) - This form is used to report your income to the state of Oklahoma. If you are required to file, you must include the credit claimed on the 538 S form.

- Federal Tax Return (Form 1040) - A copy of your federal income tax return is often needed to verify your income and household composition. It provides a comprehensive overview of your financial situation.

- Schedule for Additional Exemptions - If you have more dependents than can be listed on the 538 S form, this schedule provides the necessary details about each additional dependent.

- Proof of Residency - Documents such as utility bills, lease agreements, or bank statements may be required to confirm your residency in Oklahoma for the entire year.

- Social Security Cards for Dependents - To qualify your dependents, you may need to provide their Social Security numbers. Having copies of their cards can simplify this process.

- Income Verification Documents - Pay stubs, bank statements, or other records that demonstrate your total household income may be necessary to substantiate your claim.

- Medicaid or Aid Documentation - If you are claiming a refund based on receiving Medicaid or other aid, documentation proving this assistance may be required.

- Death Certificate (if applicable) - If a taxpayer or spouse has passed away, a death certificate may be needed to process claims for the deceased’s estate.

- Texas Real Estate Purchase Agreement - This form is essential for those engaging in property transactions, as it establishes the necessary terms and conditions for the sale. More information can be found at UsaLawDocs.com.

- Form 511RF (Request for Refund) - If you are seeking a refund for overpayment, this form should be submitted along with the 538 S form to streamline the refund process.

Gathering these documents can facilitate a smoother application process for your sales tax credit or refund. Ensure that all information is accurate and complete to avoid delays in processing your claim.

Guide to Using Oklahoma 538 S

Filling out the Oklahoma 538 S form requires careful attention to detail. This form is essential for individuals seeking a sales tax refund or credit based on their household income and exemptions. To ensure a smooth process, follow these step-by-step instructions to complete the form accurately.

- Begin by entering your first name, middle initial, and last name in the designated fields. Include your spouse's first name and initial if applicable.

- Provide your present home address, including the apartment number or rural route, city, state, and zip code.

- Fill in your Social Security Number and your spouse's Social Security Number in the appropriate sections.

- Indicate if you received Aid to Families with Dependent Children (A.F.D.C.) at any point in 1996. If yes, you are not eligible for a refund.

- Check the boxes to confirm if your address is a Nursing Home or Public Shelter and whether you were an Oklahoma resident for the entire year.

- Record the dates you lived in Oklahoma, specifying the start and end dates.

- List your dependents in the designated section, including their names, ages, Social Security numbers, relationships to you, and their income.

- Calculate the total number of exemptions claimed, including yourself, your spouse, and dependents.

- In Part I, report your total income from all sources, including wages, rental income, and other household income. Ensure to round to the nearest whole dollar.

- Sum up all household income and enter it in the specified line. If this total exceeds $12,000, you will not qualify for a credit or refund.

- If your household income is $12,000 or less, move to Part II and calculate your sales tax credit based on the number of exemptions claimed.

- Sign and date the form, ensuring both you and your spouse (if applicable) have signed it.

- Submit the completed form with your Oklahoma Individual Income Tax Return or mail it to the Oklahoma Tax Commission by the required deadlines.

After completing the form, ensure that all information is accurate and complete to avoid delays in processing. If you are required to file an income tax return, remember to claim the credit on your tax return. For those not required to file, submit the form directly to the Oklahoma Tax Commission by June 30th following the close of the taxable year.