Fill in a Valid Oklahoma 561Nr Template

The Oklahoma 561NR form is a critical document for part-year residents and nonresidents seeking to claim capital gain deductions on their Oklahoma tax returns. This form allows individuals to report qualifying capital gains and losses that are included in their federal adjusted gross income. It specifically addresses capital gains from various sources, including the sale of real or tangible personal property located within Oklahoma, stock or ownership interests in Oklahoma-based entities, and gains from installment sales. To qualify for the deduction, certain holding periods must be met—assets must generally be held for at least two or five uninterrupted years, depending on the type of asset. Additionally, the form requires detailed information, such as descriptions of the property sold, acquisition dates, sale prices, and costs. Taxpayers must also provide supporting documentation, including copies of relevant federal forms like Schedule D and Form 6252. By completing the 561NR accurately, taxpayers can ensure they take full advantage of the capital gain deductions available under Oklahoma law.

Document Properties

| Fact Name | Description |

|---|---|

| Form Purpose | The Oklahoma 561NR form is used to claim the capital gain deduction for part-year residents and nonresidents of Oklahoma. |

| Qualifying Assets | Assets must be held for a minimum of two or five years, depending on the type of property, to qualify for the deduction. |

| Governing Law | The form is governed by Title 68 O.S. Section 2358 and Rule 710:50-15-48. |

| Required Attachments | Taxpayers must attach relevant federal forms, such as Federal Form 6252 and Federal Form 4797, when filing. |

| Capital Loss Carryover | A capital loss carryover from previous years can reduce current year gains from qualifying property. |

| Net Capital Gain Calculation | To determine the net capital gain, taxpayers must subtract any capital losses from their qualifying gains. |

Common mistakes

-

Incomplete Information: Many people fail to fill out all required fields on the Oklahoma 561NR form. Missing essential details, such as property descriptions or dates of acquisition and sale, can lead to delays or rejections. It’s important to double-check that every section is filled out completely.

-

Incorrect Financial Figures: Entering incorrect amounts for sales prices, costs, or gains can create significant issues. Always ensure that the figures you report match those on your Federal Schedule D. Miscalculating these numbers could result in an inaccurate capital gain deduction.

-

Not Enclosing Required Forms: Failing to attach necessary supporting documents, such as Federal Forms 6252 or 4797, is a common oversight. These documents provide crucial context and verification for your reported gains. Without them, your form may not be processed correctly.

-

Ignoring Holding Period Requirements: Each type of asset has specific holding period requirements to qualify for deductions. Many individuals overlook these rules, leading to disqualified gains. It’s vital to ensure that the assets sold meet the necessary timeframes before the sale.

Popular PDF Documents

Oklahoma Unemployment Maximum Weekly Benefit 2023 - A variety of services are offered, including job referrals and skills enhancement programs.

When engaging in a property transaction in Texas, having a well-structured Texas Real Estate Purchase Agreement form is essential, as it lays down the necessary terms and conditions for the sale. It is imperative to utilize accurate resources to draft this document, and for comprehensive information, you can visit UsaLawDocs.com.

Oklahoma Tax Commission Forms - Recipients may choose between direct deposit into checking or savings accounts based on their preference.

Misconceptions

- Misconception 1: The Oklahoma 561NR form is only for full-year residents.

- Misconception 2: All capital gains are eligible for the deduction.

- Misconception 3: The form can be submitted without any supporting documents.

- Misconception 4: Losses can be claimed without restrictions.

- Misconception 5: Only individuals can claim the deduction.

- Misconception 6: The deduction is automatic upon filing.

- Misconception 7: The 561NR form is the same as the regular 511 form.

- Misconception 8: Filing the form is optional if there are no gains.

This form is specifically designed for part-year residents and non-residents who have capital gains from Oklahoma sources. It allows these individuals to report and potentially deduct qualifying capital gains.

Not all capital gains qualify. Only those from specific assets held for the required duration—either two or five years—are eligible. The type of asset and its holding period determine eligibility.

Supporting documentation is essential. Taxpayers must enclose copies of relevant federal forms, such as Federal Form 6252 for installment sales or Federal Form 4797 for business property sales.

While capital losses can offset gains, they are subject to specific reporting requirements. Taxpayers must list losses in the appropriate sections and ensure they are sourced to Oklahoma.

Pass-through entities, such as partnerships and S corporations, can also qualify. However, individual members must meet the holding period requirements for the entity's assets to be eligible.

Taxpayers must actively calculate their deduction based on the information provided on the form. They need to compare net capital gains and losses to determine the appropriate deduction amount.

While both forms deal with income tax, the 561NR is specifically tailored for non-residents and part-year residents, focusing on capital gains and losses unique to their situations.

If a taxpayer has any Oklahoma-sourced capital gains or losses, they must file the 561NR form, even if the net result is zero. This ensures compliance with state tax regulations.

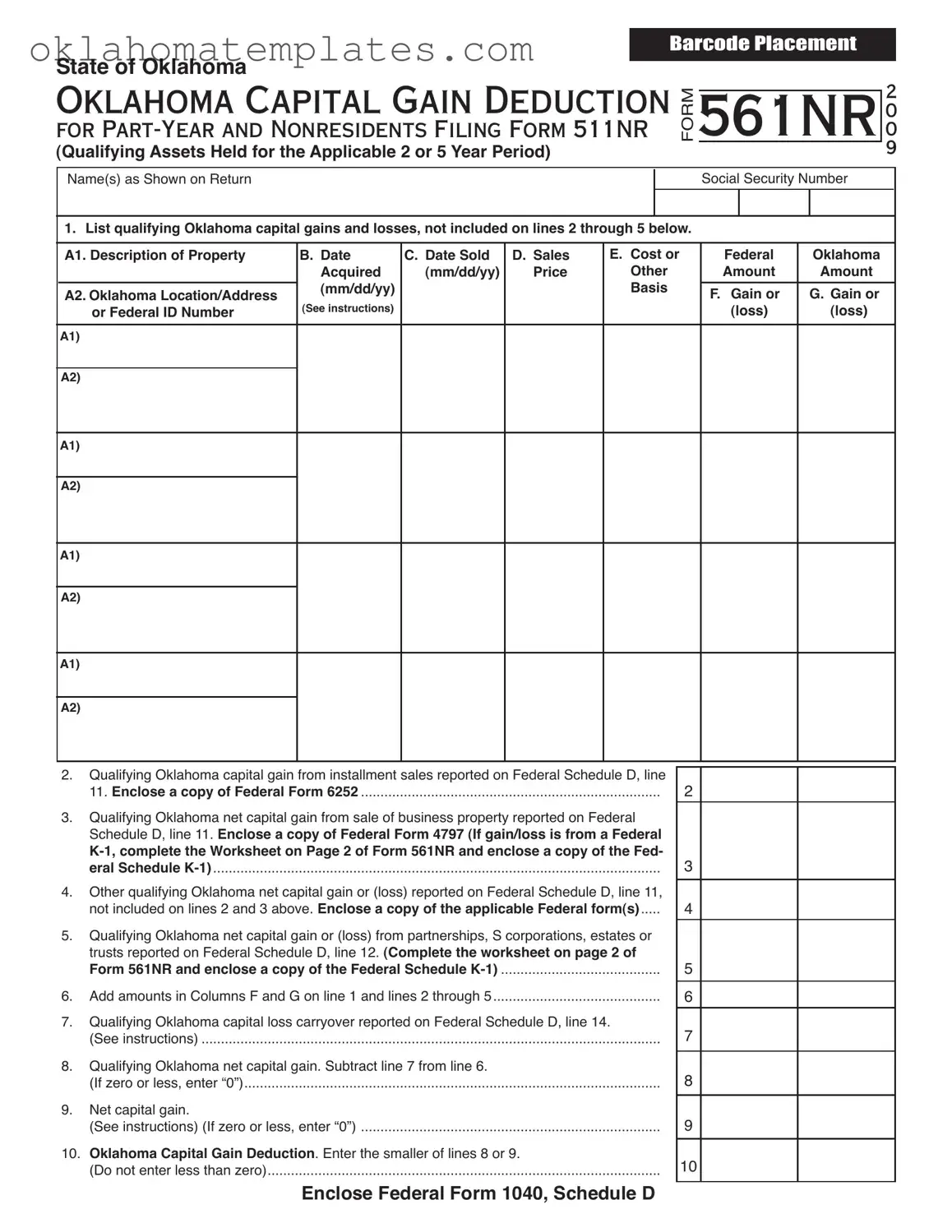

Preview - Oklahoma 561Nr Form

State of Oklahoma

BARCODE PLACEMENT

OKLAHOMA CAPITAL GAIN DEDUCTION

FOR

(Qualifying Assets Held for the Applicable 2 or 5 Year Period)

FORM

561NR

2

0

0

9

Name(s) as Shown on Return |

|

|

|

|

|

Social Security Number |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. List qualifying Oklahoma capital gains and losses, not included on lines 2 through 5 below. |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

A1. Description of Property |

B. Date |

C. Date Sold |

D. Sales |

E. Cost or |

Federal |

|

Oklahoma |

||

|

Acquired |

(mm/dd/yy) |

Price |

Other |

Amount |

|

Amount |

||

A2. Oklahoma Location/Address |

(mm/dd/yy) |

|

|

Basis |

F. Gain or |

|

G. Gain or |

||

|

|

|

|

|

|

||||

or Federal ID Number |

(See instructions) |

|

|

|

|

(loss) |

|

(loss) |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

A1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2.Qualifying Oklahoma capital gain from installment sales reported on Federal Schedule D, line 11. Enclose a copy of Federal Form 6252 .............................................................................

3.Qualifying Oklahoma net capital gain from sale of business property reported on Federal Schedule D, line 11. Enclose a copy of Federal Form 4797 (If gain/loss is from a Federal

4.Other qualifying Oklahoma net capital gain or (loss) reported on Federal Schedule D, line 11, not included on lines 2 and 3 above. Enclose a copy of the applicable Federal form(s).....

5.Qualifying Oklahoma net capital gain or (loss) from partnerships, S corporations, estates or trusts reported on Federal Schedule D, line 12. (Complete the worksheet on page 2 of Form 561NR and enclose a copy of the Federal Schedule

6.Add amounts in Columns F and G on line 1 and lines 2 through 5...........................................

7.Qualifying Oklahoma capital loss carryover reported on Federal Schedule D, line 14.

(See instructions) ......................................................................................................................

8.Qualifying Oklahoma net capital gain. Subtract line 7 from line 6.

(If zero or less, enter “0”)...........................................................................................................

9.Net capital gain.

(See instructions) (If zero or less, enter “0”) .............................................................................

10.Oklahoma Capital Gain Deduction. Enter the smaller of lines 8 or 9.

(Do not enter less than zero).....................................................................................................

2

3

4

5

6

7

8

9

10

Enclose Federal Form 1040, Schedule D

Form 561NR - Page 2

BARCODE PLACEMENT

OKLAHOMA CAPITAL GAIN DEDUCTION

FOR

Title 68 O.S. Section 2358 and Rule

Worksheet - (Enclose with Form 561NR)

Name(s) as Shown on Return

Social Security Number

FORM 561NR WORKSHEET FOR (CHECK ONE): LINE 3

OR LINE 5

Complete a separate worksheet for each piece of property sold. Enclose a copy of the Federal Schedule

Name of

Description of property sold: ______________________________________________________________________

Location of property: ____________________________________________________________________________

Date acquired: ______________________________________ Date sold: __________________________________

Date(s) you acquired ownership in the

General Information

Individual taxpayers can deduct qualifying gains receiving capital gain treatment which are included in Federal adjusted gross income. “Qualifying gains receiving capital treatment” means the amount of net capital gains, as deined under Internal Revenue

Code Section 1222(11). The qualifying gain must result from:

1.the sale of the real or tangible personal property located within Oklahoma that has been owned for at least ive uninter- rupted years prior to the date of the transaction that gave rise to the capital gain;

2.the sale of stock or an ownership interest in an Oklahoma company, limited liability company, or partnership where such stock or ownership interest has been owned for at least two uninterrupted years prior to the date of the transaction that gave rise to the capital gain; or

3.the sale of real property, tangible personal property or intangible personal property located within Oklahoma as part of the sale of all or substantially all of the assets of an Oklahoma company, limited liability company, or partnership or an Oklahoma proprietorship business enterprise where such property has been owned by such entity or business enter- prise or owned by the owners of such entity or business enterprise for a period of at least two uninterrupted years prior to the date of the transaction that gave rise to the capital gain.

An Oklahoma company, limited liability company, partnership or proprietorship business enterprise is an entity whose primary headquarters has been located in Oklahoma for at least three uninterrupted years prior to the date of sale.

A capital loss carryover from qualiied property reduces the current year gains from eligible property.

Capital gain from qualifying property, as described above, held by a

deduction, provided the individual has been a member of the

prior to the date of the transaction that created the capital gain. The type of asset sold, as shown in

tion to the individual identifying the

Installment sales...

Qualifying gains included in an individual taxpayer’s Federal adjusted gross income for the current year which are derived from installment sales are eligible for exclusion, provided the appropriate holding periods are met.

Speciic Instructions

Line 1:

List qualifying Oklahoma capital gains and losses from Federal Schedule D, line 8 or from Federal Schedule

Column A, line A1 enter the description of the property as shown in Federal Column A and on line A2 enter either the Oklahoma location of the real or tangible personal property sold or the Federal Identiication Number of the company, limited liability

Form 561NR - Page 3

OKLAHOMA CAPITAL GAIN DEDUCTION FOR

Title 68 O.S. Section 2358 and Rule

Speciic Instructions - continued

company or partnership whose stock or ownership interest was sold. Complete Columns B through F using the information from the corresponding columns of the Federal Schedule D or

In Column G enter the qualifying Oklahoma capital gains and losses reported in Column F which were sourced to Oklahoma on Form 511NR, line 7 “Oklahoma Amount” column.

Line 2:

Column F: If Federal Form 6252 was used to report the installment method for gain on the sale of eligible property on the Fed- eral return, compute the capital gain deduction using the current year’s taxable portion of the installment payment. Enclose Fed- eral Form 6252. Capital gain from an installment sale is eligible for the Oklahoma capital gain deduction provided the property was held for the appropriate holding period as of the date sold.

In Column G enter the capital gain from an installment sale of eligible property reported in Column F which was sourced to Okla- homa on Form 511NR, line 7 “Oklahoma Amount” column.

Line 3:

Column F: Enter the qualifying Oklahoma net capital gain from the Federal Form 4797 which was reported on Federal Schedule D. Enclose a copy of the Federal Form 4797. If reporting a gain/loss from a Federal Schedule

In Column G enter the other qualifying Oklahoma capital gain from Federal Form 4797 reported in Column F which was sourced to Oklahoma on Form 511NR, line 7 “Oklahoma Amount” column.

Line 4:

Column F: Enter other qualifying Oklahoma capital gains reported on Federal Schedule D, line 11. Enclose the applicable Fed- eral form(s). If not shown on the Federal form, enclose a schedule identifying the type and location of the property sold, the date of the sale, and the date the property was acquired.

In Column G enter the other qualifying Oklahoma capital gains reported in Column F which were sourced to Oklahoma on Form 511NR, line 7 “Oklahoma Amount” column.

Line 5:

Column F: Enter qualifying Oklahoma net capital gain or loss from partnerships, S corporations, trusts and estates. Complete the worksheet on page 2 of Form 561NR and enclose a copy of the Federal Schedule

In Column G enter the qualifying Oklahoma net capital gain or loss from

Line 7:

Column F: Enter the total qualifying Oklahoma capital loss carryover from the prior year’s return.

In Column G enter the qualifying Oklahoma capital loss carryover reported in Column F which was sourced to Oklahoma on Form 511NR, line 7 “Oklahoma Amount” column.

Line 9:

Column F: The Oklahoma capital gain deduction, in the “Federal Amount” column, may not exceed the net capital gain included in Federal adjusted gross income. The term “net capital gain” means the excess of the net

Column G: The Oklahoma capital gain deduction, in the “Oklahoma Amount” column, may not exceed the portion of the net capital gain sourced to Oklahoma. This is the net capital gain from Form 511NR, line 7 “Oklahoma Amount” column. If there is no net capital gain, enter “0”.

Note: The net capital gain must be decreased for any capital gain or increased for any capital loss from the sale of state and municipal bonds exempt from Oklahoma income tax.

Line 10:

Column F: Compare lines 8 and 9. Enter the smaller amount here and on Form 511NR, Schedule

Column G: Compare lines 8 and 9. Enter the smaller amount here and on Form 511NR, Schedule

FAQ

What is the purpose of the Oklahoma 561NR form?

The Oklahoma 561NR form is designed for part-year residents and nonresidents who are filing Form 511NR. It allows individuals to claim a capital gain deduction for qualifying assets sold during the tax year. This deduction applies to gains from the sale of real or tangible personal property located in Oklahoma, or from the sale of stock or ownership interests in Oklahoma-based entities, provided certain ownership periods are met.

Who qualifies to use the Oklahoma 561NR form?

Individuals who are part-year residents or nonresidents of Oklahoma can use the 561NR form if they have capital gains from qualifying assets that were owned for the required duration. Specifically, property must be held for at least five uninterrupted years for real or tangible personal property, or two uninterrupted years for stocks and ownership interests. Additionally, if the gains are derived from a pass-through entity, the individual must have been a member of that entity for the applicable holding period.

What information do I need to provide on the Oklahoma 561NR form?

When filling out the Oklahoma 561NR form, you will need to provide detailed information about each qualifying asset sold. This includes the description of the property, the dates acquired and sold, the sales price, and the cost basis. You will also need to report any qualifying capital gains or losses from installment sales, business property, and partnerships. It's essential to enclose any relevant federal forms, such as Form 6252 or Form 4797, as required.

How does the capital gain deduction work on the Oklahoma 561NR form?

The capital gain deduction allows taxpayers to reduce their taxable income by the amount of qualifying net capital gains. To determine the deduction, you will need to calculate your total qualifying gains and subtract any capital loss carryovers from previous years. The deduction is limited to the smaller of the net capital gain included in your federal adjusted gross income or the portion of the net capital gain sourced to Oklahoma. If the result is zero or less, you will enter “0” for the deduction.

Documents used along the form

When preparing the Oklahoma 561NR form, you may also need to gather additional documents to ensure a complete and accurate filing. Here are four commonly used forms that complement the 561NR:

- Federal Form 1040: This is the standard individual income tax return form used by U.S. citizens and residents. It reports your total income, deductions, and credits, and is essential for determining your overall tax liability.

- Federal Schedule D: This form is used to report capital gains and losses from the sale of assets. It helps you calculate your net capital gain or loss, which is crucial when determining the amounts to include on the 561NR.

- Federal Form 6252: If you have sold property using the installment method, this form is necessary. It reports income from the sale of property over time, which can affect your capital gains calculation on the 561NR.

- Missouri Operating Agreement Form: For those establishing or managing an LLC, the key Missouri Operating Agreement insights help to define management roles and procedures effectively.

- Federal Form 4797: This form is used to report the sale of business property. If you have sold business assets, you will need to include this form to calculate any qualifying capital gains for the 561NR.

Having these documents ready will help streamline the process of completing your Oklahoma 561NR form. Ensure you review each form carefully to provide accurate information and maximize your potential deductions.

Guide to Using Oklahoma 561Nr

Completing the Oklahoma 561NR form requires careful attention to detail, as it involves reporting capital gains and losses for part-year and non-residents. Following these steps will ensure that the form is filled out accurately and submitted correctly.

- Gather Required Information: Collect all necessary documents, including Federal Forms 1040, Schedule D, and any relevant federal forms such as 6252 and 4797.

- Fill in Personal Information: Enter your name(s) as shown on your tax return and your Social Security number at the top of the form.

- List Qualifying Gains and Losses: On line 1, provide descriptions of qualifying Oklahoma capital gains and losses. Include the acquisition date, sale date, sales price, cost or basis, and gain or loss amounts in the respective columns.

- Include Installment Sales: For line 2, report any qualifying Oklahoma capital gain from installment sales. Ensure you enclose a copy of Federal Form 6252.

- Report Business Property Sales: On line 3, enter the qualifying Oklahoma net capital gain from business property sales as reported on Federal Form 4797. Attach a copy of this form.

- Document Other Gains: For line 4, list any other qualifying Oklahoma net capital gain or loss reported on Federal Schedule D, enclosing the applicable federal forms.

- Include Partnerships and S Corporations: On line 5, provide details for qualifying gains or losses from partnerships, S corporations, or trusts. Complete the worksheet on page 2 of Form 561NR and include a copy of the Federal Schedule K-1.

- Calculate Total Gains: Add the amounts from Columns F and G on line 6 to determine the total qualifying Oklahoma capital gains.

- Account for Capital Loss Carryovers: On line 7, report any qualifying Oklahoma capital loss carryover from the previous year.

- Determine Net Capital Gain: Subtract the amount on line 7 from line 6 to find your qualifying Oklahoma net capital gain on line 8. If the result is zero or less, enter “0”.

- Calculate Net Capital Gain: Complete line 9, ensuring that if the result is zero or less, you enter “0”.

- Calculate Oklahoma Capital Gain Deduction: On line 10, enter the smaller amount of lines 8 or 9, ensuring not to enter less than zero.

- Review and Submit: Double-check all entries for accuracy. Enclose all required federal forms and submit the completed Oklahoma 561NR form with your state tax return.